if

?

FOR INFORMATION

?

S.97-60

SIMON FRASER UNIVERSITY

?

MEMORANDUM

TO:

Senate

FROM:

Alison Watt

Director, Secretariat. Services

DATE:

August 28, 1997

SUBJECT:

Annual Financial Statement

Section 31 of the University Act states: "The board shall make an annual report of

its transactions to the Minister, in which shall be set out a balance sheet and a

statement of revenue and expenditure for the year ending on the preceding March

. ?

31, and other particulars the Minister may require. A copy of the annual report shall

be transmitted promptly to the senate."

A copy of the report is attached.

NOTE:

IF YOU DO NOT WISH TO KEEP THE ANNUAL FINANCIAL STATEMENT,

PLEASE RETURN IT TO BOBBIE GRANT, OFFICE OF THE REGISTRAR.

S.

. .

SIMON FRASER UNIVERSITY

FINANCIAL STATEMENTS ?

FOR THE YEAR ENDED MARCH 31, 1997

0.

..

SIMON FRASER UNIVERSITY

FINANCIAL STATEMENTS

MARCH 31, 1997

TABLE OF CONTENTS

Page

1. Statement of Management Responsibility

?

1

2.

Report of the Vice-President Finance & Administration

?

2

3.

Report of the Auditor General

?

5

• •

?

4. Audited Statements

- Balance Sheet

?

6.

- Statement of Revenue, Expenses and Changes in Operating Equity

?

7

- Statement of Changes in Financial Position

?

.

? 8

5. Notes to the Financial Statements

?

9

0.

STATEMENT OF MANAGEMENT RESPONSIBILITY

The University is responsible for the preparation of the financial statements and has

prepared them in accordance with generally accepted accounting principles for not-for

profit organizations. The financial statements present fairly the financial position of the

University as at March 31, 1997 and the results of its operations for the year then

ended.

In fulfilling its responsibilities and recognizing the limits inherent in all systems, the

University has developed and maintains a system of internal control designed to

provide reasonable assurance that University assets are safeguarded from loss and

that the accounting records are a reliable basis for the preparation of financial

statements.

The Board of Governors carries out its responsibility for review of the financial

statements principally through its Audit Committee. The majority of the members of the

Audit Committee are not officers or employees of the University. The Audit Committee

meets with Management and the external auditors to discuss the results of audit

examinations and financial reporting matters. The external auditors have full access to

the Audit Committee, with and without the presence of Management.

The financial statements for the year ended March 31, 1997 have been reported on by

the Auditor General of the Province of British Columbia, the auditor appointed under the

University Act. The Auditor's Report outlines the scope of his examination and provides

his opinion on the fairness of presentation of the information in the financial statements.

David P. Gagan, ?

R.W. Ward

Acting President

?

Vice President, Finance &

Administration

Page 1

.•

Government Grants

Student fees

Investment income

Other income

Total Revenue

Expenses

119,443

119,104

119,635

39,756

40,743

39,361

3,543

4,442

4,114

3,012

3,003

3,275

165,754

167,292

166,385

S E

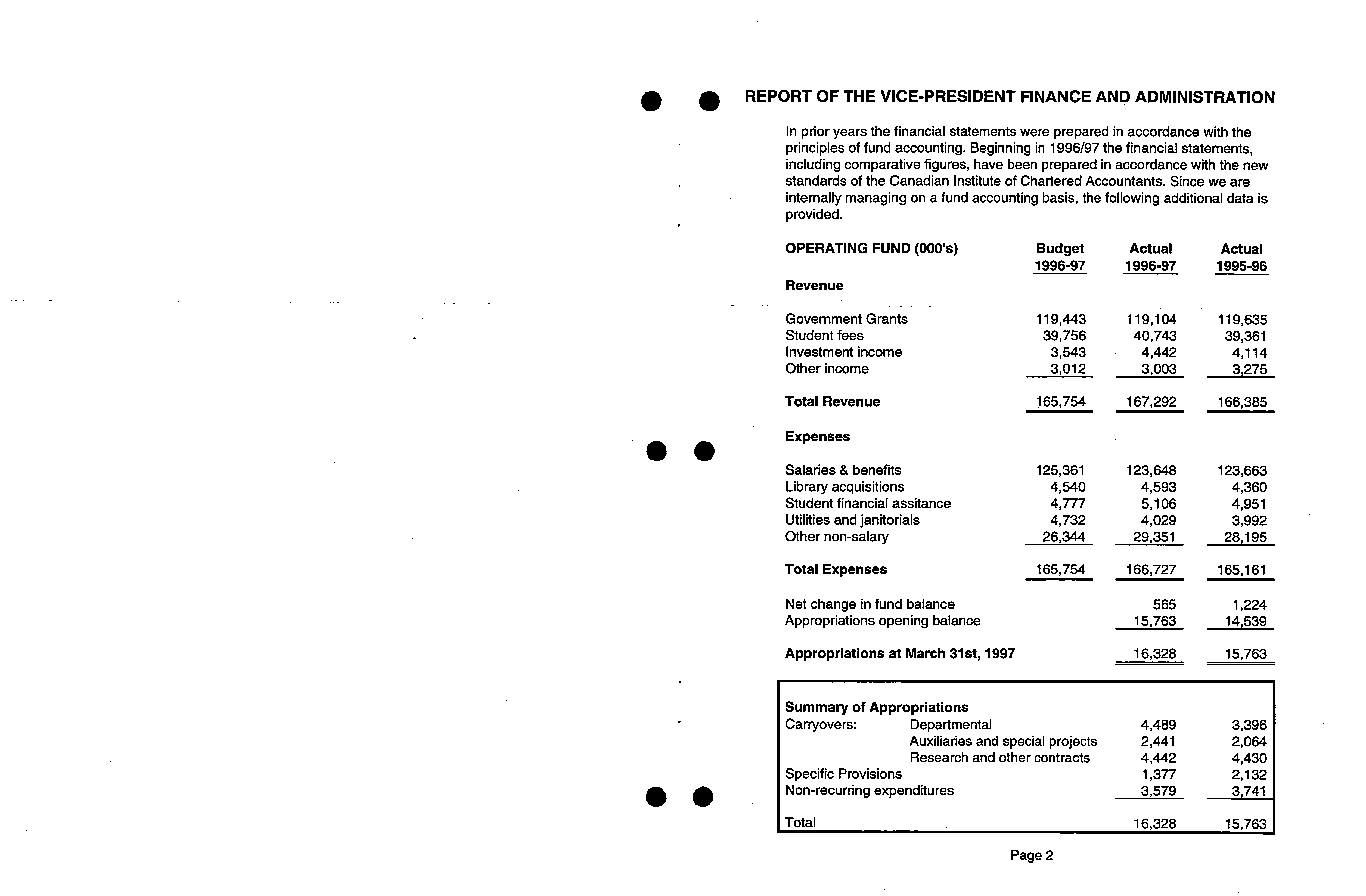

. • REPORT OF THE VICE-PRESIDENT FINANCE AND ADMINISTRATION

In prior years the financial statements were prepared in accordance with the

principles of fund accounting. Beginning in 1996/97 the financial statements,

including comparative figures, have been prepared in accordance with the new

standards of the Canadian Institute of Chartered Accountants. Since we are

internally managing on a fund accounting basis, the following additional data is

provided.

OPERATING FUND (000's)

?

Budget

?

Actual

?

Actual

1996-97 ?

1996-97 ?

1995-96

Revenue

125,361

123,648

123,663

4,540

4,593

4,360

4,777

5,106

4,951

4,732

4,029

3,992

26,344

29,351

28,195

165,754

166,727

165,161

565

1,224

15,763

14,539

16,328

15,763

Salaries & benefits

Library acquisitions

Student financial assitance

Utilities and janitorials

Other non-salary

Total Expenses

Net change in fund balance

Appropriations opening balance

Appropriations at March 31st, 1997

Summary of Appropriations

Carryovers:

?

Departmental

?

4,489 ?

3,396

Auxiliaries and special projects

?

2,441

?

2,064

Research and other contracts

?

4,442 ?

4,430

Specific Provisions

?

1,377 ?

2,132

[i

?

-

Non-recurring expenditures

?

3,579 ?

3,741

Total

?

16,328 ?

15,763

Page 2

• ?

The latest actuarial valuation as at December 31, 1993 showed an actuarial liability of

$64,440,000 and assets on hand of $70,770,000 resulting in a surplus of $6,330,000. As

recommended by the Actuary, the rate of employer contribution was changed from 9.42%

to 9.56% of annual earnings effective January 1, 1995. The next actuarial valuation will be

completed prior to December 31, 1997. The assets and liabilities of both pension plans are

not reflected in the financial statements.

14. Contingent Liabilities

Simon Fraser University is the defendant to several unresolved statements of claims. It is

not expected that the ultimate outcome of these claims will have a material effect on the

financial position of the University.

15. Comparatives

Certain comparative figures have been restated to conform with the current year's

presentation.

.

This statement reflects the format of the 1996/97 Operating Budget, approved by

the Board of Governors in June of 1996. The summary of appropriations of

$16,328 has been extracted from Note 10 to the Financial Statements.

Operating Fund

In comparison to budget, operating revenues have increased by .93%. A cash

reduction of $548,000 was made to the operating grant mid-year by the Prov-

ince, while an addition of $209,000 for Pay Equity, applicable for increases proc-

essed in 1995/96, was made to the base. Student fees are increased due to in-

creased undergraduate and graduate enrollment, and as a result of continued

growth in the non-credit areas of Executive Business and Professional, Writing

and Applied Science programs. Investment income is improved following a rally

in the bond market that has allowed for favourable capital gains. The University

continues to provide additional support from the operating budget for library ac-

quisitions and student financial assistance, and this is reflected in the increase in

expenditures over that of 1995/96. For a more complete analysis and commen-

tary on revenues and for detail on expenditure line items, the 1996/97 Year-end

Results and the 1997/98 Operating Budget are available at www.sfu.calfinance

under 1997/98 Approved Operating Budget

Ancillary Enterprises

Included in Ancillary Enterprises are the Bookstore, Food Services, Residences,

Parking Operations and the Microcomputer Store. The Bookstore and the Micro-

computer Store were relocated to the new Maggie Benston Building during the

year. Parking Operations installed a Parking Operation Management System

which allows for daily update and tracking of all lot activity. The Ancillary Fund

surplus of $484,000 is used by individual ancillaries for future upgrades to facili-

ties, equipment replacement and for new service initiatives, such as the installa-

tion of security cameras in the parking lots.

Research

Grants for the National Centre of Excellence for Teleleaming increased by $1.6

million. The Teleleaming project involves approximately 130 researchers from

Canadian universities who are involved in 56 research projects across 7 themes.

There was $23 million of externally funded research activity during the year, an

increase of $1 million over 1995/96.

Endowment.

This fund increased by $20 million; $15 million is related to the Burnaby Land

Endowment.

Page 3

. .

. .

Page 20

amount of income that may be expended, and reinvesting unexpended income. Included

?

Specific Purpose

in the $71,851 are the following receivables:

Consisting of specific projects such as those funded by the Canadian Interna-

tional Development Agency, the sources of specific purpose funds include gov-

ernment grants, conference fees and interest income from endowments. This

fund also includes scholarships funded through endowment income. Activity in

the fund this year was $21 million, similar to that of 1995/96.

Capital

SFU Foundation

?

$9,985,000

?

Proceeds from future sale of 29 lots

City of Burnaby

?

4,000,000

?

$1 million a year over the next 4 years

Government of B.C.

?

850,000

?

Matching Fund Program

13. Pension Plans

Academic Pension Plan

The University pension plan for academic staff generally provides benefits on a money

purchase basis, but includes an option to members who were in the plan on March 20,

1973 to choose benefits based on years otservice, and the. average of the highest sixty

(60) consecutive months' salary.

An amendment to the plan in 1981 and a letter of agreement between the University and

the Faculty Association in 1990 addressed the funding and the distribution of the formula

retirement benefit account. The latest actuarial valuation of this account as at January 1,

1995 estimates an unfunded liability of $1,112,000 to be funded over the next 7 ½ years.

The University is making annual contributions of $195,000 per year as of 1995 until the

liability for past service is fully funded. The new current service contribution, estimated to

be $142,000 for 1995, is 1.2% of members' earnings. As of January 1996 the 1.2% is paid

bi-weekly to the pension fund.

Administrative/Union Pension Plan

The University Pension Plan for the Administrative/Union staff provides benefits based on

years of service and the average of the highest sixty (60) consecutive months' salary. A

revised plan dated January 1, 1993 is still under review by Revenue Canada. Under the

revised plan:

a.

The University's contribution is based on the amounts estimated by the Actuary and

recommended by the administrative /union pension plan Trustees to the Board of

Governors of the University. The University shall contribute to the fund such

amounts as the Board of Governors determines are required to fund the retirements

benefits and other plan benefits.

b.

The University shall not suspend or reduce its contribution to the pension fund

without the prior approval of the employee organizations.

C. ?

Any surplus in excess of a contingency reserve equal to 15% of the liabilities is to be

distributed to members via separate money-purchase accounts maintained with the

fund.

.O

The Maggie Benston Student Services Centre, funded by both the university and

the Simon Fraser Student Society, was completed this year. Following the move

to this building, limited renovations have been made to the Academic Quadran-

gle and Strand Hall. A mid-year adjustment by the Province resulted in a reduc-

tion in funding for renovations by $2.1 million. Funding for cyclical renewal and

maintenance was reduced by $1.1 million. A recent Memorandum of Under-

standing with the City of Burnaby will allow Simon Fraser University to develop

market housing; in exchange for a transfer of 771 acres to the City of Burnaby,

Simon Fraser University received approval for the development, residential lots

valued at $10 million, and $5 million to be paid over five years. The $15 million

Burnaby Land Endowment will be established using these funds.

Page 4

Page 19

To the Members of the Board of Governors

of Simon Fraser University:

VIctorzq, British Columbia

June 6, 1997

The capital reserve represents funds that are committed to capital projects.

The funds committed for specific purpose are set aside to meet the cost of future

obligations.

a.

Group insurance funds are designated for potential requirements related to self-

insured group life and long-term disability plans. Annual premiums are funded from

the general operating funds on a cost of claim plus fee for services basis.

b.

Lease commitment funds provide for commitments entered into for the occupancy of

the University's Harbour Centre facility which include lease payments, tenant loan

payments and a contribution towards operating costs. Lease and tenant loan

obligations include annual payments of $1,140,00, which started in September 1988

increasing to $1,648,000 over the term of the lease, and a termination payment of

$8,000,000 upon the expiry of the lease in December 2017 or a discounted

equivalent of that amount at an earlier date.

C. ?

Self-insurance funds are held to pay self-insured property and liability losses.

11.

Equity in Capital Assets

?

?

1997

?

1996

S •

?

( 000) ?

(000)

Opening equity in capital assets

?

71,411 ?

$68,551

Net investment in capital assets

?

5,729

?

2,860

Land disposal ?

(987) ?

-

• Equity in capital assets

?

$761 53

?

$71 .411

12.

Endowment Principal

?

1997 ?

1996

?

(000) ?

(000)

Balance, beginning of year

?

$51,112 ?

$44,888

Donations

?

18,390 ?

3,615

Capitalized income and other transfers

?

2,349

?

2.609

Balance, end of year as per financial statements

?

$71,851

?

$0...112

Endowment consists of restricted donations to the University. The investment income

generated from endowments must be used in accordance with the various purposes

established by the donors or the Board of Governors. Donors as well as University policy

stipulate that the economic value of the endowments must be protected by limiting the

91%

Report of the Auditor General?

of British Columbia

I have audited the balance sheet of

Simon Fraser University

as at March 31, 1997 and the

statements of revenue, expenses and changes in operating equity and of changes in

financial position. These financial statements are the responsibility of the University's

management. My responsibility is to express an opinion on these financial statements

based on my audit.

I conducted my audit in accordance with generally accepted auditing standards. Those

standards require that I plan and perform an audit to obtain reasonable assurance whether

the financial statements are free of material misstatement. An audit includes examining,

on a test basis, evidence supporting the amounts and disclosures in the financial statements.

An audit also includes assessing the accounting principles used and significant estimates

made by management, as well as evaluating the overall financial statement presentation.

In my opinion, these financial statements present fairly, in all material respects, the

financial position of the

Simon Fraser University

as at March 31, 1997 and the results of its

operations and changes in its financial position for the year then ended in accordance with

generally accepted accounting principles.

Page 18

SIMON FRASER UNIVERSITY

Statement

.

BALANCE SHEET

AS AT MARCH

31, 1997

9. ?

Changes in Equity

?

.

•

•

(thousands of dollars)

Equity in

1997

1996

Capital Endowment

?

1997

1996

.

?

ASSETS

Operating Reserves Assets

?

Principal

?

Total

Total

(000) ?

(000) ?

(000) ?

(000) ?

(000)

(000)

,

CURRENT

Cash

ASSETS

and short-term investments

$

?

33,826

?

$

19

Balance, beginning of year

?

$(2,400)

?

$44,493 ?

$71,411

?

$51,112 ?

$164,616

$151,978

Accounts receivable

31,262

18,263

Excess of revenue over

Prepaid expenses

827

1,093

expenses ?

(200) ?

- ?

- ?

- ?

(200)

(200)

Inventories

3,074

2,584

Endowment contributions ?

-

?

- ?

- ?

18,390

?

18,390

3,615

INVESTMENTS

68,989

21,959

Capitalized income and

Long-term investments (Note 4)

95,517

115,329

other transfers

? - ?

- ?

- ?

2,349 ?

2,349

2,609

Deferred charges

2,144

2,472

Internally imposed restrictions

?

697

?

4,742

?

-

?

5,349-

6,614--

CAPITAL ASSETS (Note 5)

298,003

296,995

Balance, end of year

?

$(2600) ?

$45190

?

$76153 ?

$71851 ?

$190594

$164616

10

?

Reserves ?

1997

1996

$464 653 ?

$

436,755

General Operating ?

(000)

(000)

LIABILITIES AND EQUITY

Carryovers - faculties & departments

?

$ 4,489

$

3,396

CURRENT LIABILITIES

Auxiliaries and special projects

?

2,441

2,064

Accounts payable and accruals

$ ?

24,471 ?

$

23,374

Research and other grants ?

4,442

4,430

Current portion of long term debt (Note 6)

8,367

7,990

Specific provisions

?

1,377

2,132

Non-recurring expenditures

?

3,579

3,741

LONG TERM LIABILITIES

Total General Operating

?

16,328

15,763

175,808

1

Loans

Ancillary enterprises ?

1,887

1,198

Deferred contributions (Note 8)

58

873

53,326

274,059

272,139

Capital ?

7,245

8,323

Funds committed for specific purposes

EQUITY (Note 9)

-Group insurance ?

2,924

2,700

Operating

(2,600)

(2,400)

-Lease commitment ?

16,323

16,015

Reserves (Note

10)

45,190

44,493

-Self insurance ?

483

494

Capital assets (Note

11)

76,153

71,411

Endowment (Note

12)

71,851

51,112

TOTAL RESERVES

?

$45,190

190594

164,616

The general operating reserves are composed of carryover funds for faculties and

$464,653 ?

$

436,755

departments under a policy that allows faculties to carryover unspent instructional salaries

and also allows departments to carry over up to

$25,000

of unspent non-salary

budget.

These reserves also include unspent balances on specific projects and intemally funded

The accompanying notes are an integral part of these financial statements

research already in progress and, funds set aside for specific provisions and one-time non-

recurring expenditures as approved by the Board of Governors.

Approvel:

The ancillary enterprise reserve represents accumulated funds held for the ongoing

operations of ancillaries such as the Bookstore, Food Services, Microcomputer

Store,

1/

J \

OLA

Residences and Parking.

I

D.E(Bond, Ph.D.

R.W. Ward, Ph.D.

Page 17

Chair

Vice President

Board of Governors

Finance and Administration

Page 6

SIMON FRASER UNIVERSITY

Statement

STATEMENT OF REVENUE, EXPENSES

and

CHANGES IN OPERATING EQUITY

•

Loans Payable

FOR THE YEAR

(thousands

ENDED

of dollars)MARCH

31,

1997

Loans payable consist of:

?

1997

.

?

1996

.

.

?

(000) ?

(000)

1997

1996

C

Interim financing

?

$2,140

?

$5,227

REVENUE

I

Tuition

Government

and related

grants

feesand

contracts

$ ?

167,88446,828

$

?

170,847

44,561

Revolving loans

?

4,400

?

1,000

Gifts, grants and contracts

11,693

9,264

Total

?

$6.540 ?

$6.227

Sale of goods and services

?

.

20,488

. ?

20,128

Investment income

9,025 ?

:

7,707

The interim financing is for capital projects, as authorized by the provisions of the

Miscellaneous income

6,630

5,962

Educational Institution Capital Finance Act and the Financial Administration Act, and will be

Amortization of deferred capital contributions

8,279

7,723

replaced by long-term debt The revolving loans are authorized under Section 55 of the

University Act.

270,827

266,192

8.

Deferred Contributions

EXPENSESalaries

-

-

other

academicinstruction

and research

24

56,695819

23,662

57,079

1997

(000)

?

?

1996

(000)

-

support staff

52,319

51,935

Total salaries

133,833

132,676

Balance, beginning of year

?

$ 53,326 ?

$ 50,769

Employee benefits

22,280

21,423

Contributions received during the year ?

276,374 ?

268,749

Travel and personnel costs

8,453

7,984

• •

Transferred to revenue ?

270,827 ?

266,192

Supplies and expenses

18,276

18,750

Grants

Depreciationto

other agencies

21,3102,727

19,381

1,519

Balance, end of year ?

$_58,873 ?

$_

53,326

Equipment and facility rentals

4,627

4,647

Utilities

3,303

3474

The balance is made up of the following

Scholarships, fellowships and bursaries

8,196

7,794

Sponsored Research ?

$ 8,259

?

$

8,288

Contract services

3,014

3,004

Specific Purpose

?

17,408 ?

14,520

Professional fees

4,411

4,106

Capital ?

33,206

?

30,518

Renovations and alterations

2,581

2,538

Cost

Debt

of

servicing

goods sold-

interest

22739

9,838

22,421

10,061

TOTAL DEFERRED CONTRIBUTIONS

?

$58-373

?

$51326

265,588

259,778

Under the deferred method of accounting for contributions, restricted contributions related

NET INCOME

5,239

6,414

to expenses of future periods are deferred and recognized as revenue in the period in

which the related expenses are incurred. The $33,206,000 of deferred capital contribution

CHANGES IN EQUITY

represents the "unamortized" portion of restricted capital grants and repayment of debt

Increase in reserves

(697)

(3,754)

relating to assets which were purchased with restricted contributions, but which still have

Investment in capital assets

(4,742)

(2,860)

an undepreciated book value.

NET (DECREASE) INCREASE DURING YEAR

(200)

(200)

OPERATING EQUITY, beginning of year

(2,400)

(2,200)

OPERATING EQUITY, end of year

$ ?

(2,600)

$(2,400)

Page 16

Page 7

present values required to fund repayment of the debentures at maturity. The

debentures can be recalled by the Authority upon notice of not less than five

months. Sinking fund and interest payments are made with funds received from the

Province of British Columbia for that purpose. Annual sinking fund and interest

payments due within the next five fiscal years are as follows:

(000)

1998 ?

$27441

SIMON FRASER UNIVERSITY

Statement

1999 ?

$26280

STATEMENT OF CHANGES IN FINANCIAL POSITION

2000 ?

$25,674

2001 ?

$24,658

'

FOR THE YEAR ENDED MARCH 31,

1997

2002

?

$22,937

thousands of dollars

b.

?

Canada Mortgage and Housing

Corporation

Annual Payments

1997

1996

--Interest ?

Balance Outstanding

- ?

- ?

-

CASH PROVIDED BY (USED i) OPERATING ACTIVITIES

Maturity Date ?

Rate

?

1997 ?

1996

Until Maturity

Excess of revenue over expense ?

$

5,239 ?

$

6,414

(0O0'

' ?

/

?

?

(000

' ?

'

'000

'

?

'

Depreciation

21,310

19,381

Net decrease (increase) in non-cash current assets

(13 223)

(2,185)

Jan

1 ?

2017 ?

5375% ?

$

151 ?

$ ?

155

$ 12

Net increase (decrease) in current liabilities

1,474

(2,859)

Jan 1: 2018 ?

5 875% ?

778

?

796

65

Amortization of deferred capital contributions

(8,279)

(7,723)

Jul

?

1, ?

2019

?

6.875%

?

1,940 ?

1,976

171

6,521

13,028

2.869 ?

$2-327

$24

CASH PROVIDED BY (USED IN) INVESTING ACTIVITIES

The debentures are secured by a floating charge on the Madge Hogarth, Shell

Net decrease (increase) in long term investments

19,812

(29,382)

House and Louis Riel student residences respectively. The residences

are recordedW

?

W

Capital asset acquisitions

(22,318)

(34,732)

on the balance sheet at a cost of $6,361,000.

C. ?

The Province of British Columbia (Minister of Finance and

Corporate

(2,506)

(64,114)

Relations)

Annual Payments

CASH PROVIDED BY (USED IN) FINANCING ACTIVITIES

Interest ?

Balance Outstanding

(incl. interest)

Net increase (decrease) in long term debt and loans payable

(4,773)

10,959

Maturity Date ?

Rate ?

P ?

1997

-

?

1996

Until Maturity

Increase in deferred contributions

13,826

7,886

I

?

(000)

(000)

Endowment contributions

20,739

6,224

Jan. 18, ?

1999 ?

5.40% ?

$2,120

?

2,120

269

29,792

25,069

Jan. ?

9, ?

2002 ?

9.00% ?

3,000 ?

3,000

336

INCREASE IN CASH AND SHORT TERM INVESTMENTS

33,807

(26,017)

Sep

Jan. ?

9

?

2012

?

9.500Y(o ?

3,0001

?

3,000

2,

350

CASH AND SHORT TERM INVESTMENTS, beginning of year

19

26,036

A ?

,

20 ?

8

?

/O

CASH AND SHORT TERM INVESTMENTS, end of year ?

$

33,826 ?

$

19

$ 26313 ?

$26.444

$2946

The debenture maturing in 2005 is secured by a floating charge on the McTaggart

Cowan student residence. The residence is recorded on the balance sheet at a cost

of $3,685,000.

The remainder are bonds which were issued to finance capital expenditures on a

parkade and student residences.

Page 15

Page 8

1.

b.

C.

SIMON FRASER UNIVERSITY

5.

. .

Capital Assets

?

997

.

NOTES TO THE FINANCIAL STATEMENTS

1997 ?

Accumulated

?

1997

Cost

?

Depreciation

?

Net

?

1996

FOR THE YEAR ENDED MARCH 31, 1997

(000) ?

(000) ?

(000) ?

(000)

Buildings-

?

284,735 ?

75,469 ?

209,266 ?

208,094

Authority and Purpose

f

Site Services

??

.

21,818 ?

5,269 ?

16,549 ?

16,775

Leasehold Improvements ?

10,302 ?

2,281 ?

8,021 ?

8,360

Simon Fraser University (SFU) operates under the authority of the University Act of British

Equipment & Furnishings

?

. ?

79,145 ?

36,427 ?

42,718 ?

43,790

Columbia. We are a comprehensive research university offering a full range of •

'

Library Acquisitions

?

32,533

?

11,656 ?

20,877

?

18,417

undergraduate, graduate and continuing studies programs. The academic governance of

Land

?

572 ?

- ?

572 ?

1.559

the University is vested in the Senate. We are a not-for-profit entity, governed by a Board

of Governors, the majority of which are appointed by the provincial government of British

Total Capital Assets

?

$429.105

?

$131.102

?

$298003

?

$296.995

Columbia. We are a registered charity and are therefore exempt from income taxes under

Section

149

of the Income Tax Act.

The original

1,200

acres of campus land were granted or donated to the University in

1965. As

at March

31", 1996

it was recorded on the balance sheet at

$1,559,000

based

Summary of Significant Accounting Policies and Reporting Practices

on the Municipality of Burnaby assessment at the date of donation. During the fiscal year a

net total of

771

acres was given back to the City of Burnaby in exchange for

$5,015,000

in

General

cash and land, in the form of residential lots, valued at

$9,985,000.

An amount of

$1,015,000

was received in

1996/97

with the remaining balance to be received at the rate

of $1,000,000 per year over the next four years. The land valued at

$9,985,000

was

In prior years the financial statements were prepared in accordance with the principles of

transferred by the City of Burnaby to the SFU Foundation and the cash will be transferred

fund accounting. Starting in

1996/97

the financial statements, including comparative

to the University as the Foundation sells the lots. This

$15,000,000 will

become an

figures, have been prepared in accordance with the new standards of the Canadian

endowment fund. The remaining

429

acres is recorded in the financial statements at its

Institute of Chartered Accountants (CICA) Accounting Standards Board. These new

1965

assessed value of

$572,000.

standards for "not for profit organizations" result in significant changes for financial

• • ?

6.

Long-Term Debt

statements prepared by universities and SFU has adjusted its accounting policies

accordingly. The impact of the changes are contained in Note 3.

Long-term debt consists of the following:

1997

?

1996

Accounting Method

(000) ?

(000)

British Columbia Educational

Starting in fiscal

1996/97,

the financial statements are prepared on a non-fund basis as the

Institutions Capital

Financing

Authority ?

$206Y'968 ?

$206,779

operations for the entire entity have been combined for reporting purposes. The university

Less: sinking fund ?

149,564 ?

45,201

follows the accrual basis of accounting. Unrestricted revenue is recorded when receivable

157,404

?

161,578

and expenditures are recorded when goods or services are received.

Canada Mortgage and Housing

Corporation ?

2,869 ?

2,927

Revenue Recognition

Province-of-British Columbia

?

26,313

?

26,444

Less: Sinking fund

?

2,411 ?

1.737

Operating grants are recognized in the period when receivable. Operating grants received

26,771 ?

27.634

184,175 ?

189,212

for a future period are deferred until that future period and are reflected as deferred

Less: Current portion

?

8.367 ?

7.990

contributions.

Total ?

$175,808

?

$181.222

Amounts

revenue at

received

the time

for

the

tuition

goods

fees

are

and

delivered

sales of

or

goods

the services

and services

are provided.

are recognized

Otherwise,

as

these

a. ?

Authority

British Columbia Educational Institutions Capital Financing

amounts are classified as unearned revenue in accounts payable.

These debentures are issued to the British Columbia Educational Institutions Capital

Externally restricted contributions for purposes other than endowment or the acquisition of

Financing Authority under the Educational Institution Capital Finance Act, bearing

interest

?

from

5.40%

to

17.00%

capital assets are deferred and recognized as revenue in the year in which the related

at rates

?

and maturing from

1998

to

2024.

Payments

to the sinking fund, which is.held by the Authority, are based on the discounted

3.

a.

Page

9

?

Page

14

4.

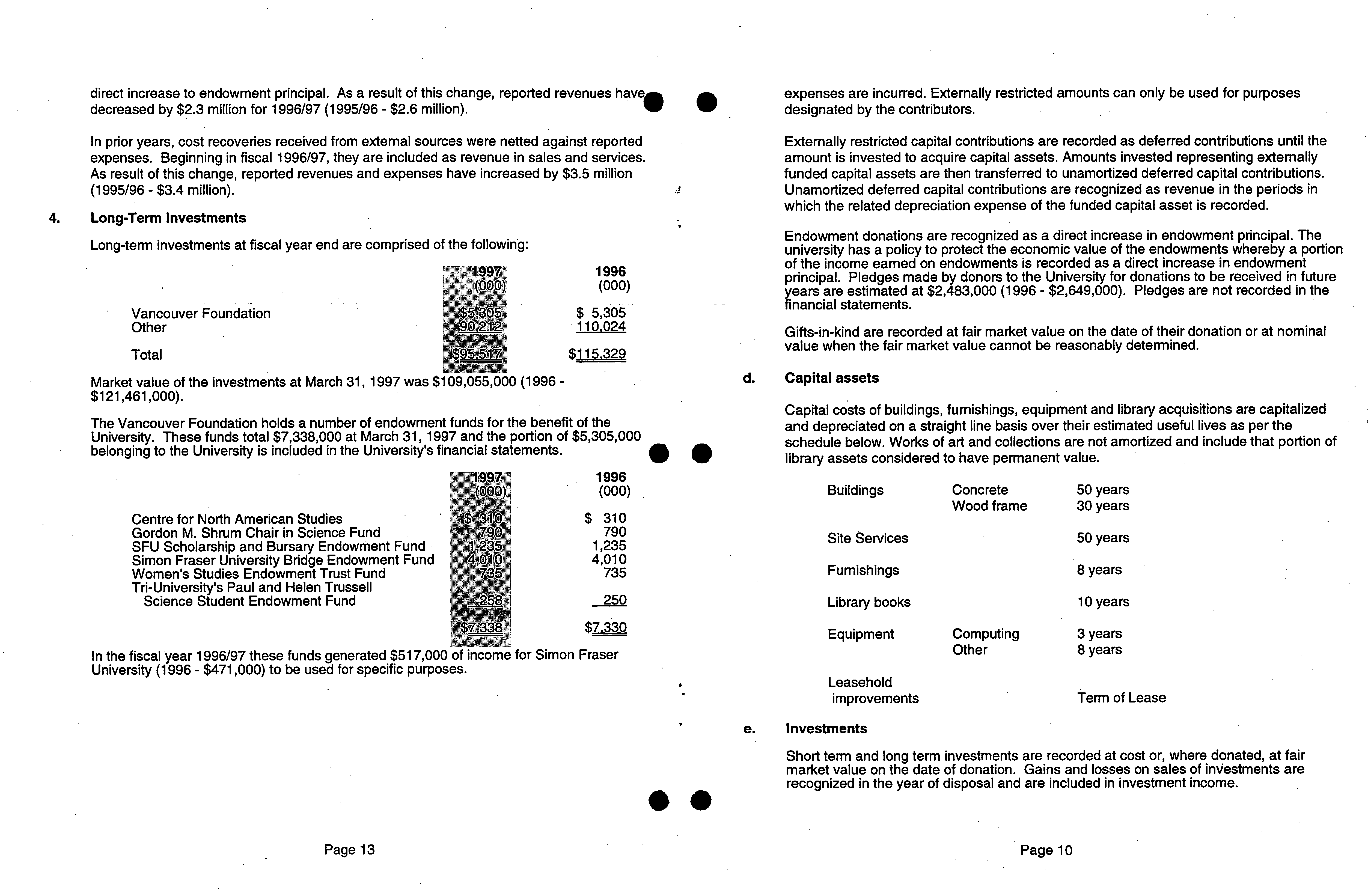

direct increase to endowment principal. As a result of this change, reported revenues have

decreased by $2.3 million for 1996/97 (1995/96 - $2.6 million).

In prior years, cost recoveries received from external sources were netted against reported

expenses. Beginning in fiscal 1996/97, they are included as revenue in sales and services.

As result of this change, reported revenues and expenses have increased by $3.5 million

(1995/96 - $3.4 million).

?

J

Long-Term Investments

Long-term investments at fiscal year end are comprised of the following:

1997

1996

(000)

(000)

Vancouver Foundation

?

$5 305

$ 5,305

Other

?

90212

110,024

Total

?

$95,517

$115,329

Market value of the investments at March 31, 1997 was $109,055,000 (1996 -

$121,461,000).

The Vancouver Foundation holds a number of endowment funds for the benefit of the

University. These funds total $7,338,000 at March 31, 1997 and the portion of $5,305,000

belonging to the University is included in the University's financial statements.

?

• •

expenses are incurred. Externally restricted amounts can only be used for purposes

designated by the contributors.

Externally restricted capital contributions are recorded as deferred contributions until the

amount is invested to acquire capital assets. Amounts invested representing externally

funded capital assets are then transferred to unamortized deferred capital contributions.

Unamortized deferred capital contributions are recognized as revenue in the periods in

which the related depreciation expense of the funded capital asset is recorded.

Endowment donations are recognized as a direct increase in endowment principal. The

university has a policy to protect the economic value of the endowments whereby a portion

of the income earned on endowments is recorded as a direct increase in endowment

principal. Pledges made by donors to the University for donations to be received in future

years are estimated at $2,483,000 (1996 - $2,649,000). Pledges are not recorded in the

financial statements.

Gifts-in-kind are recorded at fair market value on the date of their donation or at nominal

value when the fair market value cannot be reasonably determined.

d.

?

Capital assets

Capital costs of buildings, furnishings, equipment and library acquisitions are capitalized

and depreciated on a straight line basis over their estimated useful lives as per the

schedule below. Works of art and collections are not amortized and include that portion of

library assets considered to have permanent value.

.

1997

1996

(000)

(000)

Buildings

Concrete

50 years

Wood frame

30 years

Centre for North American Studies

-310

$

$ 310

Gordon

SFU Scholarship

M. Shrum

and

Chair

Bursary

in Science

Endowment

Fund

Fund

1,235

790

1,235

790

Site Services

50 years

Simon Fraser University Bridge Endowment Fund

4-,010

4,010

Women's Studies Endowment Trust Fund

735

735

Furnishings

8 years

Tr-University's Paul and Helen Trussell

Science Student Endowment Fund

,

258

250

Library books

10 years

'$7338

$7330

Equipment

Computing

3 years

In the fiscal year 1996/97 these funds generated $517,000 of income for Simon Fraser

Other

8 years

University (1996 - $471,000) to be used for specific purposes.

Leasehold

improvements

Term of Lease

e.

?

Investments

Short term and long term investments are recorded at cost or, where donated, at fair

market value on the date of donation. Gains and losses on sales of investments are

recognized in the year of disposal and are included in investment income.

S.

Page 13

?

Page 10

f.

g.

h.

Financial Instruments

?

single shareholder. At March 31, 1997 the Foundation is holding residential lots

valued at $9,985,000 and the proceeds from the sale of those lots will be transferred

The estimated fair value of cash, cash equivalents, accounts receivables and accounts

?

to the University. It also received a building valued at $2,250,000 whose ownership

payables approximates carrying value due to the relatively short-tern, nature of the

?

will be transferred to the University in the coming year. Assets and liabilities of the

instruments.

?

?

Simon Fraser University Foundation amounting to $12,694,249 and $10,349,050

respectively are not included in the financial statements of the University.

At the date of these financial statements, it is not practicable within constraints of

timeliness and cost to determine the fair value of sinking funds and debt. The majority of

?

3. CHANGES IN ACCOUNTING POLICY, PRESENTATION PRACTICE AND PRIOR

sinking funds and debt is held by British Columbia Educational Institutions Capital

?

PERIOD ADJUSTMENTS

Financing Authority (a crown corporation). The Province of British Columbia guarantees

the debt and provides annual appropriations to pay interest and sinking fund provisions on

?

a. ?

Presentation Practice

the debt.

Inventories ?

In

prior years, the financial statements were prepared in accordancëwith the principles of

fund accounting. Commencing in fiscal 1996/97 and applied retroactively to 1995/96, the

Inventories of supplies kept at Central Stores are recorded at cost. Inventories of

?

financial statements are prepared on a non-fund basis as the operations for the entire

merchandise held for resale in the Bookstore and the Microcomputer Store are recorded at

?

entity have been combined for reporting purposes.

the lower of cost and net realizable value.

b. ?

Depreciation of Capital Assets

University Interests in WCUMBS, TRIUMF, SFUV and SFU Foundation

The University is one of five university members of the Western Canadian

Universities Marine Biological Society (WCUMBS) which operates a research station

at Bamfield, British Columbia. The University's annual operating grant to the

Society remains the same as last year at $158,000 and is recorded as an

expenditure by the university. The accounts of WCUMBS are not included in these

statements other than that initial contributions in the amount of $347,000 for capital

acquisitions, are recorded as capital assets on the Balance Sheet. There is no

expectation of monetary gain to the University from this venture.

The University is one of four parties to a joint venture agreement under which

research is conducted by University faculty members at the Tr-Universities Meson

Facility (TRIUMF) on the University of British Columbia campus and elsewhere. The

facility and its operations are funded by federal government grants and the

University makes no direct financial contribution. The accounts of TRIUMF are not

included in these statements. There is no expectation of monetary gain to the

University from this venture.

iii.

The University owns 100% of the shares of SF Univentures Corporation (SFUV),

which was established to promote technology transfer to the private sector. The

consolidated assets of SFUV are not considered to be material and are not included

in these financial statements.

iv.

The Simon Fraser University Foundation was established in 1987 under the

provisions of the University Foundations Act. Its main purpose is to receive,

British

manage

Columbia

and invest

through

funds

the

to

Minister

further

of

the

Finance

purposes

and Corporate

of the University.

Relations

The

is the

Province of •

•

In prior years, purchases of capital assets were initially recorded as an expense against

the fund in the year of acquisition. The value of capital assets capitalized, net of any

outstanding debt related to those assets, was credited to equity in capital assets. No

depreciation was recorded. Equipment was written off in full after 8 years, while buildings

would have been written off only upon demolition.

In fiscal 1996/97, the University changed its policy of capitalizing assets. Capital costs of

buildings, furnishings, equipment, library acquisitions and debt repayment are no longer

recorded as expenses in the year of acquisition or payment. They are now capitalized and

depreciated over their estimated useful lives as detailed in Note 2(d).

This change has the effect of decreasing reported expenses by $13.7 million (1995/96 -

$26.0 million) and decreasing the reported Capital Assets and Equity in capital assets by

$163.1 million (1995/96 -$147.9 million).

C. ?

Revenue Recognition

In prior years, contributions were recognized as revenue when received. During the year,

the University changed to the accounting policy described in Note 2(c). This change has

had the effect of decreasing reported revenues by $11.8 million (1995/96 - decreasing by

$21.1 million). On the balance sheet it has had the effect of increasing deferred

contributions and reducing equity by $58.8 million (1995/96 - $53.3 million).

In prior years, the portion of endowment income which is capitalized was recorded as

revenue and subsequently transferred to endowment principal as an interfund transfer.

Beginning in fiscal 1996/97 the investment income which is capitalized is recognized as a

Page 11

?

Page 12