S.04-77

0 ?

FOR INFORMATION

?

(Formerly S.04-67)

SIMON FRASER UNIVERSITY

?

MEMORANDUM

TO: ?

Senate

FROM: ?

Alison Watt

Director, University Secretariat

DATE: ?

September 16, 2004

SUBJECT:

Annual Financial Statements

Section 32 of the University Act states: "The board must make an annual report of its

transactions to the minister, in which it must set out a balance sheet and a statement of revenue

and expenditure for the year ending on the preceding March 31, and other particulars the minister

.

?

may require. A copy of the annual report shall be transmitted promptly to the senate."

NOTE:

IF YOU DO NOT WISH TO KEEP THE ANNUAL FINANCIAL STATEMENT, PLEASE?

RETURN IT TO BOBBIE GRANT, OFFICE OF STUDENT SERVICES/REGISTRAR

9

S.

. .

SIMON FRASER UNIVERSITY

Back to top

FINANCIAL STATEMENTS

FOR THE YEAR ENDED MARCH 31, 2004

.

?

SIMON FRASER UNIVERSITY

FINANCIAL STATEMENTS

MARCH 31, 2004

?

TABLE OF CONTENTS

Page

1.

Statement of Management Responsibility

?

1

2.

Report of the Vice-President Finance & Administration

?

2

3.

Report of the Auditor General of British Columbia

?

6

S

?

4. Audited Statements

- Statement of Financial Position

?

7

-

Statement

of Operations and Changes in Operating Net Assets

?

8

-

Statement

of Changes in Net Assets

?

9

- Statement of Cash Flows

?

10

5. Notes to the Financial Statements

?

0

?

11

0 [1

STATEMENT OF MANAGEMENT RESPONSIBILITY

?

0

The University is responsible for the preparation of the financial statements and has

prepared them in accordance with Canadian generally accepted accounting principles

for not-for profit organizations. The financial statements present fairly the financial

position of the University as at March 31, 2004 and the results of its operations for the

year then ended.

In fulfilling its responsibilities and recognizing the limits inherent in all systems, the

University has developed and maintains a system of internal control designed to

provide reasonable assurance that university assets are safeguarded from loss and that

the accounting records are a reliable basis for the preparation of financial statements.

The Board of Governors carries out its responsibility for review of the financial

statements principally through its Audit Committee. The majority of the members of the

Audit Committee are not officers or employees of the University. The Audit Committee

meets with Management and the external auditors to discuss the results of audit

examinations and financial reporting matters. The external auditors have full access to

the Audit Committee, with and without the presence of Management.

The financial statements for the year ended March 31, 2004 have been reported on by

the Auditor General of the Province of British Columbia. The Auditor's Report outlines

the scope of his examination and provides his opinion on the fairness of presentation of

the information in the financial statements.

Michael Stevenson

?

Pat Hibbitts

President ?

Vice President

Finance & Administration

. .

Page 1

2003

(000)

$3.368

3,288?

80 ?

S3.368

$ (55)

126

S__181

5,962

5,174

3,838

250,056

- 169,041

7,356

11,768

5,517

c 74

250,056

160,296

85,622

5,174

3,910

34,411

289,413

181,519

7,320

12,662

5,531

82,381

289,413

7,092

4,206

34,411

30V'67

169,962

7,401

1 2,000

5,495

61,501

256,359

157,346

61,813

5,243

4,492

27,182

256,076

155,791

6,822

7,491

5,062

46,499

221,665

C.

..Related Entities that are not consolidated

SFU FOUNDATION

?

S.

The Simon Fraser University Foundation was established in 1987 under the provisions of the

University Foundations Act. Its main purpose is to receive, manage and invest funds to further the

purposes of the University. The Province of British Columbia through the Minister of Finance is the

single shareholder. Included in total assets in 2003 were certain residential lots held for investment

purposes. The Foundation sold all of the remaining residential lots during the current year.

REPORT OF THE VICE-PRESIDENT FINANCE AND ADMINISTRATION

The university prepares its annual financial statements according to generally accepted accounting

principles for not-for-profit organizations. The operations for the entire entity have been combined

for reporting purposes. However, we continue to manage internally on a fund basis and I am pleased

to provide this financial information for the operating fund and additional information on the other

funds in the following pages.

Actual

Operating fund (000's)

?

2002103

SFU FOUNDATION

Financial Position

Total Assets

Total Liabilities

Fund Balance

Results of Operation

Total (Loss) Revenue

Total Disbursements

Deficiency of Revenue over Expenses

S

•

The University owns all of the outstanding shares of SFU Community Corporation. SFU

Community Corporation has no business operations and its sole purpose is to act as the trustee of

SFU Community Trust.

SFU Community Trust is developing 78 acres of land on the Burnaby campus into a residential

area. The SFU Community Trust was established as a Trust under the laws of British Columbia on

July 29, 2002 and the beneficiaries of the Trust are the University and the Simon Fraser University

Foundation.

SF UNIVENTURES CORPORATION

The University owns 100% of the shares of SF Univentures Corporation (SFUV), which was

established to promote technology transfer to the private sector. The consolidated assets of SFUV

are not considered to be material and are not included in these financial statements.

d.

e.

SFU COMMUNITY CORPORATION

Revenue

Government Grants

Student fees

Investment income

Other income

Prior year appropriations

Total revenue

Expenses

Salaries & benefits

Library acquisitions

Student financial assistance

Utilities and janitorials

Other non-salary

Total

Cumulative appropriations

Summary

?

ns

Carryovers: Departmental

AuxilIaries and Special projects

Research and other contracts

Specific Provisions

Non-recurring expenditures

Total

?

18,2

?

11,679

?

1,3

?

2,246

?

122

?

9,600

2,319

34,411

45,31

?

34,411

17.

Comparatives

Certain comparative figures have been restated to conform with the current years presentation

including an adjustment of $4,554,000 from internally restricted reserves to employee future

benefits liability.

The

previously

effect

reported.

of this is to reduce the 2003 closing net asset balance by $4,554,000 for amounts

5

This statement reflects the format of the

2003/2004

operating budget, approved by the Board

of Governors in May

2003.

It groups expenses in a different format than the audited statements.

The summary of the appropriations of

$45,318

at March

31, 2004

has been extracted

from note

9

to the financial statements.

• ?

* includes prior year appropriations, transfers to operating and transfers within operating.

Page 21

?

Page 2

Page 3

16. ?

Related Entities that are not consolidated

S0

a.

Simon Fraser University is a member along with the University of Alberta, the University of British

Columbia, the University

.

of Victoria and Carleton University in a joint venture called the Tr-

Universities Meson Facility (TRIUMF) located on the UBC campus. TRIUMF is Canada's

National Laboratory for research in Particle Physics. TRIUMF is not incorporated and each

University appoints three members to a Management Board. The facility and its operations are

funded by federal government grants and the University makes no direct financial contribution. The

land and buildings are owned by UBC.

TRIUMF

2004

2003

(000)

Financial Position

Total assets

U-9 3

$ 5.496

Total Liabilities

2,243

2,501

Fund Balances - restricted

2,701

1,890

-other

1,105

5.496

Results of Operation

Revenue

53..4:.8

62,530

5 ?

5 ?

Expenses

2.359t

61,110

Excess of Revenue

overExpenses

i

$1420

b. ?

WCUMBS

The University is one of five University members of the Western Canadian Universities Marine

Biological Society (WCUMBS) which operates a research station at Bamfield, British Columbia.

The Society is a not-for-profit organization incorporated under the Society Act of British

Columbia. The University's operating grant to the Society was $190,000 (2003 - $176,000) and

is recorded as an expenditure by the University. There is no expectation of monetary gain to the

University from this venture.

S

S

O

p eratin g

Fund

Government grants from the Province of British Columbia for 2003/04 were $9,000,000 higher

than the previous year due to the one time year-end infrastructure grant of $6,500,000. The

Government of Canada continued its contribution of $4,900,000 towards the infrastructure that

supports research activities. Tuition fees revenue increased by $23,400,000 as a result of the

30% increase in tuition rate and increase in enrollment. Non-credit revenue increased to

$6,800,000 from $5,300,000 the previous year. A 30% increase also applied to other student

fees and generated an additional $900,000 of revenue. Investment income was higher than

last year by $1,800,000 due to capital gains mainly in the bond market.

Salaries and benefits increased by 10.8% in total. Salary increases, merit increases, market

adjustments and a new retention initiative accounted for approximately 4% to 5% depending on

the group and the timing of the increase. An addition of staff and faculty for SFU Surrey and

the double the opportunity initiative accounted for the remainder. An additional $1,500,000 was

required to fund the non-pension retiree benefits. A portion of the tuition increase was allocated

to scholarships, bursaries and awards. As a result, student financial assistance increased by

$2,300,000. In the non-salary category the largest increases were in materials and supplies

$800,000 and operational expenses $2,300,000.

Ancillar

y

Enterprises

Included in Ancillary Enterprises are the Bookstore, Food Services, Residences, Parking

Operations and the Microcomputer Store. Ancillary Enterprises are mandated to break even

but are allowed to retain their surpluses for future upgrades to facilities, equipment replacement

and for new service initiatives. Total reserves are $5,900,000.

The SFU Bookstores in Burnaby, Harbour Centre, and Surrey provided over $11 million worth

of books, products, academic supplies and services to the University community. The stores

also sponsored numerous campus events and provided donations to student groups. Each

month an SFU faculty author was featured in the bookstore.

Food Services on the Burnaby campus, started a $1,000,000 renovation to the Mckenzie

Cafeteria to be completed in the Summer of 2004. A new dining hall will open in September

2004 with a mandatory meal plan for the. 500 students living in the new residences.

Residences spent over $4,000,000 in capital renovations in the last three years with an

expenditure of approximately $900,000 this year. The construction of a 300-seat dining hail

and two new residence towers with 464 student rooms and 14 hotel rooms are nearing

completion. This complex will open August 31, 2004. A third residence tower scheduled for

completion in February 2005, will complete the $41.5 million residence construction project

begun in 2003. In total SFU will offer an additional 727 undergraduate residence spaces to

bring the total residence spaces available at SFU to 1,831.

The Parking Operation supports all parking lot expenses and repays the debt on the parkade.

The parking rates increased by 5% in accordance with the recommendations outlined in the

Traffic Demand Management Study.

Page 20

.Administrative/Union Pension Plan

b. The latest actuarial valuation as at December 31, 2001 showed an actuarial liability of

$112,725,000 against market value assets of $127,409,000, resulting in a surplus of

$14,684,000. This surplus is not available to the University as the University shall not

suspend or reduce its contribution to the pension fund without the prior approval of the

employee organizations. Pursuant to an agreement between the University and the

employee organizations, the portion of the surplus in excess of 15% of the defined-benefit

portion of the above liabilities with assets taken at market values would be distributed to

members.

C.

The rate of employer contribution was also increased from 11.43% to 11.44%, effective

January 1, 2002, as indicated by the 2001 actuarial valuation. Contributions by the

employer for 2004 were $6,829,000 (2003 - $6,402,000).

d. ?

The valuation is based on the 1983 Group Annuity Mortality Table using an investment rate

of return of 6.75% and an inflation rate of 2.5%.

Pension Plan for Certain Members

This plan covers seven members of the faculty and staff for whom contributions were paid to the

Teachers Insurance and Annuity Association and College Retirement Equities fund in 1971, and

that have chosen to remain in the defined contribution plan. University contributions were $95,900

in 2004 ($122,773 in 2003).

Financial Instruments

The University's financial instruments consist of cash and short '

term investments, accounts

40

receivable, investments, accounts payable and accrued liabilities and long term debt. It is

management's opinion that the University is not exposed to significant interest, currency or credit

risk arising from these financial instruments.

Pledges

Pledges made by donors to the University for donations to be received in future years are

estimated at $12,300,000 (2003 - $11,144,000). Pledges are not recorded in the financial

statements until the related donations are received by the University.

Contingencies

Simon Fraser University is the defendant to several unresolved statements of claims. It is not

expected that the ultimate outcome of these claims will have a material effect on the financial

position of the University.

Canadian University Reciprocal Insurance Exchange

The University is a member in a self-insurance co-operative in association with other Canadian

universities to provide property and general liability insurance coverage. Under this arrangement

referred to as the Canadian University Reciprocal Insurance Exchange (C.U.R.I.E.), the University

is required to share in any net losses experienced by C.U.R.I.E. The commitment was recently

renewed to December 31, 2008.

0

Ancillary Enterprises

The Microcomputer Store continues to offer an increased level of customer service to SFU by

offering on-site consultation, loaning equipment, and providing a more interactive environment

for the campus community. During the year the store negotiated significant savings for SFU for

anti-virus software and Microsoft Office. During the year the Microcomputer store continued to

manage Microsoft Office, and many other software applications used by the University. It

negotiated significant savings on Adobe, BenQ LCD & manages the Dell RPF for the campus.

Research

University research is mainly funded by the Federal agencies (National Science and

Engineering Research Council and Social Services and Humanities Research Council) and the

provincial government. In addition, over $11 million comes from private sector corporations and

from non-profit organizations. There are over 1,500 active research accounts with total activity

of over $46 million compared to $43 million the previous year. The Canada Foundation for

Innovation awarded $5.4 million for infrastructure under several categories and $8.8 million was

received from the Province of BC's Knowledge Development Fund as matching funds. The

Federal government's Canada Research Chair program awarded $2.5 million for salaries and

research purposes.

Endowment

The University's endowment consists of restricted donations to the University and internal

•

allocations,

income generated

the principal

from

of

endowments

which is required

can be

to

spent

be maintained

only in accordance

in perpetuity.

with

The

the

investment

various

purposes established by the donors or the University's Board of Governors.

The Endowment Fund investment strategy aims to maintain the purchasing power of the

original capital value of endowments for future generations. It also ensures that spending

allocations remain stable each year through the use of an income stabilization fund. The

Endowment Fund is invested in bonds and equity markets to meet this strategy over the tong

term.

This fund received $2,665,000 in new donations during the year and $2,434,000 of interest

income and other transfers was capitalized in order to protect the economic value of the

endowments. The fund stands at $102,201,000 at the end of the fiscal year.

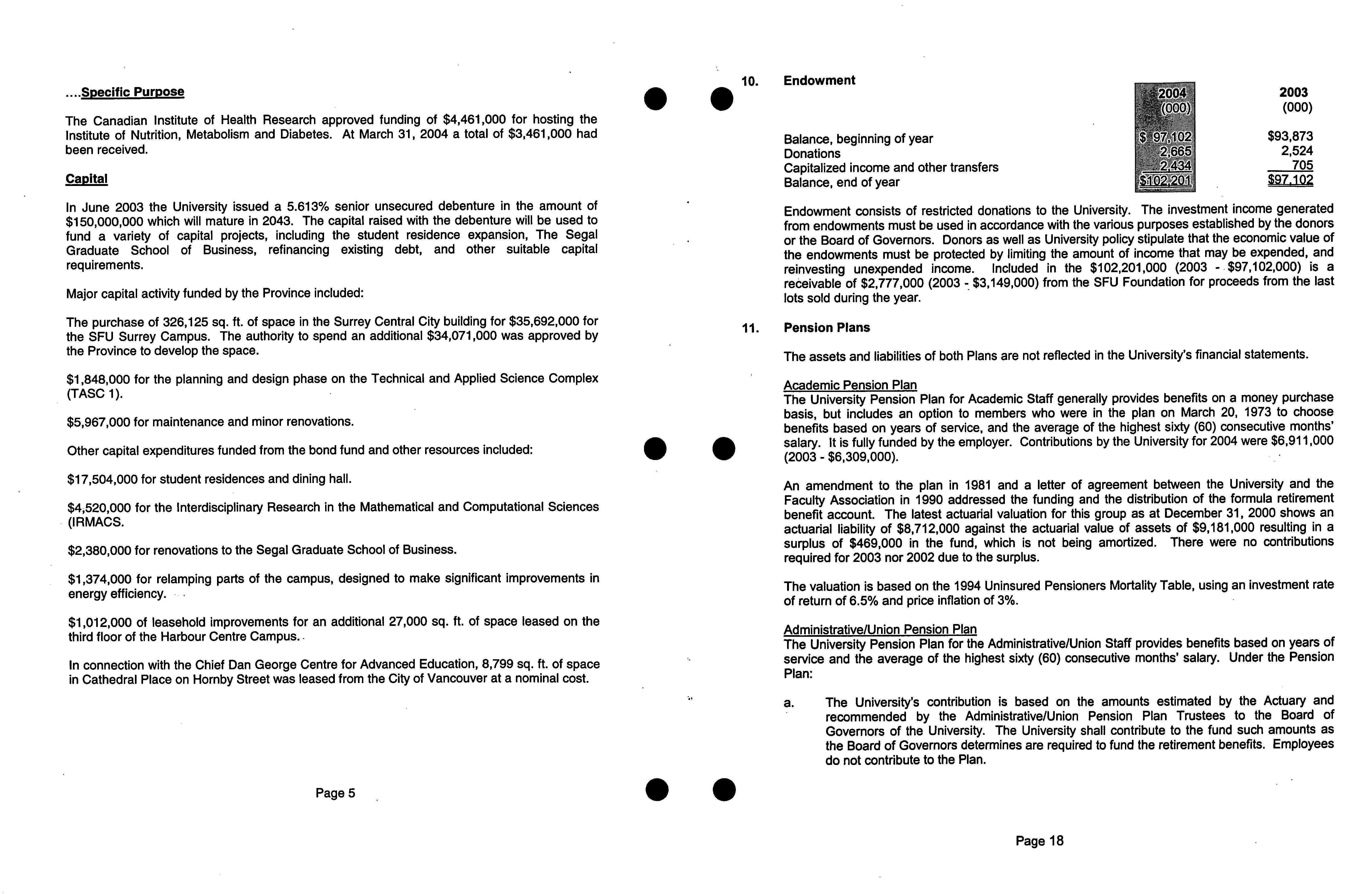

Sp

ecific Purpose

The sources of specific purpose funds include government and corporate grants, conference

fees, private donations and interest income from endowments for programs and scholarships.

There are many international activities; the Canadian International Development Agency funds

projects in China and Mexico. Field Schools funded by participants were held in Fiji, Prague,

France and Greece. The Faculty of Education also has a number of smaller international

initiatives in Jamaica and Japan.

Page 4

12.

13.

14.

15.

Page 19

.S

p ecific Purpose

10. ?

Endowment

S S

r;

:

2i1

2003

(000)1

(000)

The Canadian Institute of Health Research approved funding of $4,461,000 for hosting the

Institute of Nutrition, Metabolism and Diabetes.

?

At March 31, 2004 a total of $3,461,000 had

Balance, beginning of year

F•

?

97.1021

$93,873

been

received.

Donations

2,665

2,524

Capitalized income and other transfers

I

705

Capital

Balance, end of year

SiC2.201j

S97.102

In June 2003 the University issued a 5.613% senior unsecured debenture in the amount of

$150,000,000 which will mature in 2043. The capital raised with the debenture will be used to

fund a variety of capital projects, including the student residence expansion, The Segal

Graduate School of Business, refinancing existing debt, and other suitable capital

requirements.

Major capital activity funded by the Province included:

The purchase of 326,125 sq. ft. of space in the Surrey Central City building for $35,692,000 for

the SFU Surrey Campus. The authority to spend an additional $34,071,000 was approved by

the Province to develop the space.

$1,848,000 for the planning and design phase on the Technical and Applied Science Complex

(TASC 1).

$5,967,000 for maintenance and minor renovations.

Other capital expenditures funded from the bond fund and other resources included:

?

5

$17,504,000 for student residences and dining hall.

$4520,000 for the Interdisciplinary Research in the Mathematical and Computational Sciences

(IRMACS.

$2,380,000 for renovations to the Segal Graduate School of Business.

$1,374,000 for relamping parts of the campus, designed to make significant improvements in

energy efficiency.

$1,012,000 of leasehold improvements for an additional 27,000 sq. ft. of space leased on the

third floor of the Harbour Centre Campus.

In connection with the Chief Dan George Centre for Advanced Education, 8,799 sq. ft. of space

in Cathedral Place on Hornby Street was leased from the City of Vancouver at a nominal cost.

Endowment consists of restricted donations to the University. The investment income generated

from endowments must be used in accordance with the various purposes established by the donors

or the Board of Governors. Donors as well as University policy stipulate that the economic value of

the endowments must be protected by limiting the amount of income that may be expended, and

reinvesting unexpended income. Included in the $102,201,000 (2003 -.$97,102,000) is a

receivable of $2,777,000 (2003 - $3,149,000) from the SFU Foundation for proceeds from the last

lots sold during the year.

11. ?

Pension Plans

The assets and liabilities of both Plans are not reflected in the University's financial statements.

Academic Pension Plan

The University Pension Plan for Academic Staff generally provides benefits on a money purchase

basis, but includes an option to members who were in the plan on March 20, 1973 to choose

benefits based on years of service, and the average of the highest sixty (60) consecutive months'

salary. It is fully funded by the employer. Contributions by the University for 2004 were $6,911,000

(2003 - $6,309,000).

An amendment to the plan in 1981 and a letter of agreement between the University and the

Faculty Association in 1990 addressed the funding and the distribution of the formula retirement

benefit account. The latest actuarial valuation for this group as at December 31, 2000 shows an

actuarial liability of $8,712,000 against the actuarial value of assets of $9,181,000 resulting in a

surplus of $469,000 in the fund, which is not being amortized. There were no contributions

required for 2003 nor 2002 due to the surplus.

The valuation is based on the 1994 Uninsured Pensioners Mortality Table, using an investment rate

of return of 6.5% and price inflation of 3%.

Administrative/Union Pension Plan

The University Pension Plan for the Administrative/Union Staff provides benefits based on years of

service and the average of the highest sixty (60) consecutive months' salary. Under the Pension

Plan:

a. The University's contribution is based on the amounts estimated by the Actuary and

recommended by the Administrative/Union Pension Plan Trustees to the Board of

Governors of the University. The University shall contribute to the fund such amounts as

the Board of Governors determines are required to fund the retirement benefits. Employees

do not contribute to the Plan.

Page 5 ?

is ?

is

Page 18

.

Report of the Auditor General

?

of British Columbia

f^&N

4 W

To the Members of the Board of Governors

of Simon Fraser University, and

To the Minister ofAdvanced Education,

Province of British Columbia:

2003

(000)

•

$11,679

2,246

9,600

2,694

8,192

34,411

4,523

9,280

9,187

16,612

533

$74.546

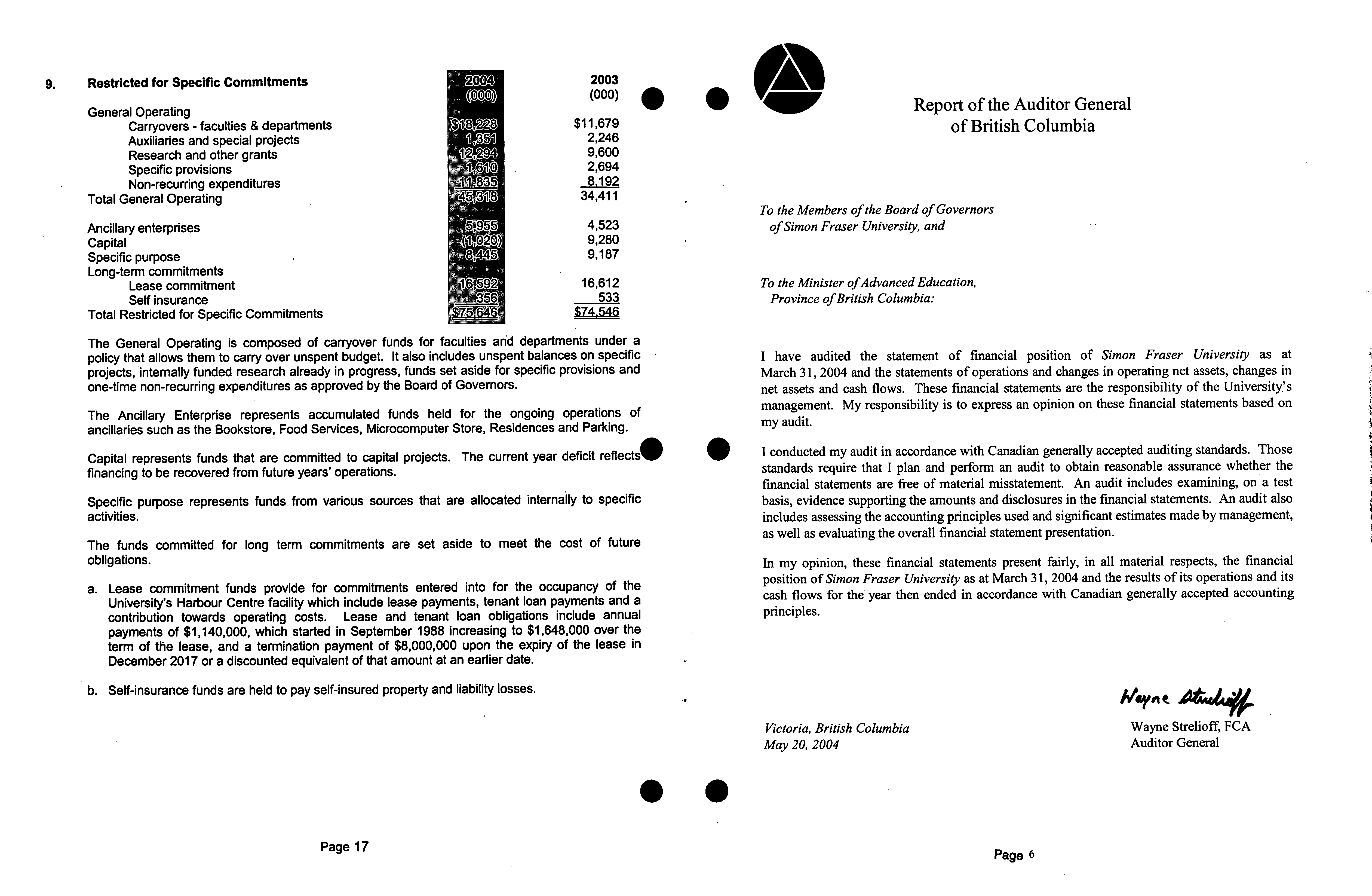

9. ?

Restricted for Specific Commitments

General Operating

Carryovers - faculties & departments

Auxiliaries and special projects

Research and other grants

Specific provisions

Non-recurring expenditures

Total General Operating

Ancillary enterprises

Capital

Specific purpose

Long-term commitments

Lease commitment

Self insurance

Total Restricted for Specific Commitments

The General Operating is composed of carryover funds for faculties and departments under a

policy that allows them to

carry

over unspent budget. It also includes unspent balances on specific

projects, internally funded research already in progress, funds set aside for specific provisions and

one-time non-recurring expenditures as approved by the Board of Governors.

The Ancillary Enterprise represents accumulated funds held for the ongoing operations of

ancillaries such as the Bookstore, Food Services, Microcomputer Store, Residences and Parking.

Capital represents funds that are committed to capital projects. The current year deficit reflectsS

?

S

financing to be recovered from future years' operations.

Specific purpose represents funds from various sources that are allocated internally to specific

activities.

The funds committed for long term commitments are set aside to meet the cost of future

obligations.

a.

Lease commitment funds provide for commitments entered into for the occupancy of the

University's Harbour Centre facility which include lease payments, tenant loan payments and a

contribution towards operating costs. Lease and tenant loan obligations include annual

payments of $1,140,000, which started in September 1988 increasing to $1,648,000 over the

term of the lease, and a termination payment of $8,000,000 upon the expiry of the lease in

December 2017 or a discounted equivalent of that amount at an earlier date.

b.

Self-insurance funds are held to pay self-insured property and liability losses.

•5

I have audited the statement of financial position of

Simon Fraser University

as at

March 31, 2004 and the statements of operations and changes in operating net assets, changes in

net assets and cash flows. These financial statements are the responsibility of the University's

management. My responsibility is to express an opinion on these financial statements based on

my audit.

I conducted my audit in accordance with Canadian generally accepted auditing standards. Those

standards require that I plan and perform an audit to obtain reasonable assurance whether the

financial statements are free of material misstatement. An audit includes examining, on a test

basis, evidence supporting the amounts and disclosures in the financial statements. An audit also

includes assessing the accounting principles used and significant estimates made by management',

as well as evaluating the overall financial statement presentation.

In my opinion, these financial statements present fairly, in all material respects, the financial

position of

Simon Fraser University

as at March 31, 2004 and the results of its operations and its

cash flows for the year then ended in accordance with Canadian generally accepted accounting

principles.

"nit 4at#

Victoria, British Columbia

?

Wayne Strelioff, FCA

May 20, 2004

?

Auditor General

Page 17

Page 6

is

•8.

$ ?

18,118

12,882

31,000

24,614

12,198

34,462

190,571

292,845

(16,928)

74,546

127,241

97,102

281,961

$574,806

Statement

I

2003 ?

.

S

$ ?

18,595

12,532

1,787

1,269

34,183

199,666 ?

340,768

?

189

$ 798,222 ?

$ 574,806

SIMON FRASER UNIVERSITY

?

STATEMENT OF FINANCIAL POSITION

AS

AT MARCH

31, 2004

?

(thousands of dollars)

ASSETS

CURRENT ASSETS

Cash and short-term investments (Note 3)

Accounts receivable

Inventories

Prepaid expenses

Investments (Note

4)

Capital assets (Note 5)

Unamortized debt discount and issue costs

LIABILITIES AND NET ASSETS

CURRENT LIABILITIES

Accounts payable and accrued liabilities

Current portion of long term debt (Note 6)

Employee future benefits (Note

7)

Long-term debt (Note 6)

Deferred contributions (Note 8)

Deferred contributions related to capital assets (Note 8)

NET ASSETS

Operating

Restricted for specific commitments (Note

9)

Invested in capital assets

Endowment (Note 10)

The accompanying notes are an integral part of these financial statements

Early Retirement

The early retirement amount represents current and future pension payments to employees that

took early retirement in the mid eighties and other employees that receive supplementary pensions.

The actuarial liability at December 31, 2003 is $4,678,000 and is fully funded.

Non-Pension Benefits

The non-pension benefits amount represents portions of premiums payable to current and future

retirees for the Medical Services Plan, Extended Health Benefits and Dental Benefits. The accrued

benefit liability for non-pension benefits is $17,609,000 (2003 -$15,085,000). At March 31, 2004

an amount of $4,790,000 has been set aside internally to fund this liability.

An actuarial valuation was done at March 31, 2003 to reflect the changes in staff and faculty and

increase in premiums since the previous valuation at March 31, 2000. The actuarial valuation

shows an increase of $7,978,000 which brings the total obligation to $23,080,000 at March 31,

2003. The increase of $7,978,000 will be amortized over the average remaining service period of

active employees. The average remaining service period of active employees covered by the non-

pension benefits as of March 31, 2004 is 9 years.

The March 31, 2003 valuation is based on the 1994 Uninsured Pensioners Mortality table. The

actuarial assumptions used in this valuation are a discount rate of 6.75%, price inflation at 2.5% per

annum, a medical trend rate of price inflation plus 3.5% and a dental trend rate of price inflation

plus 2.9%. There are no contributions by the employees to fund this benefit.

Deferred Contributions

Deferred contributions represent unspent resources externally restricted for a particular use relating

to a subsequent period. Changes in the deferred contributions are as follows:

Capital

2004

2003

Total

Total

(000) ?

(000)

(000)

$190,571

$225,033

$215,740

127,200

74,464

40003

8,453

222,121.

84,103

£268.130

65,171

$225.033

Under the deferred method of accounting for contributions, restricted contributions related to

expenses of future periods are deferred and recognized as revenue in the period in which the

related expenses are incurred. The $222,121,000 of deferred capital contribution represents the

unamortized portion of restrictecI capital advances relating to assets which were purchased with

restricted contributions.

Sponsored ?

Specific

Rearch

?

Purpose

(0,00)

my

(000)

Balance beginning of

?

II

the year

Add: Contributions

received during the year

?

34,362

?

Less: Transferred

to revenue

?

29.39 1

?

Balance end of year

E ? -

B. Louie

Chair

Board of Governors

P. Hibbitts

Vice President

Finance and Administration

.

S

Page 16

Page 7

Non-Pension?

Benefits

(000)

$15,085?

871 ?

1,572 ?

567

?

18,095 ?

486?

$17.609

Total

2003

(000)

$23,089

S

25,344?

730?

$24.6 14

Statement 2

...

Debentures,

Long Term

issued

Debt

?

to the Province of British Columbia pursuant to the Financial Administrative Act,

5

bear interest rates from 6.0% to 9.5%, and mature between 2005 and 2022.

Annual payments including principal and interest due within the next five years are as follows:

Total

(000)

2005

?

$11,487

2006

?

$11,768

2007

?

$11,077

2008

?

$11,077

2009

?

$13,487

7.

?

Employee Future Benefits

?

Group

?

Early?

Insurance Retirement

?

(000)

?

(000)

Opening Balance

?

$4,975?

Current Costs

Interest on benefit obligation

?

354

?

391

Amortization of Net?

Actuarial Loss

?

4,908

?

5,366

Disbursements

?

402

?

$4.908

?

$4.964?

GrouD Insurance

Group insurance is designated for potential requirements related to self-insured long-term disability

plans. Annual premiums are funded from the general operating funds on a cost of claim plus fee

for services basis.

a

The last actuarial valuation at March 31, 2003 for the self-insured long term disability plans shows a

liability of $5,073,000. There has been no material change in the number of employees on LTD

since that date.

The amount of $4,908,000 has been set aside internally to fund this liability.

SIMON FRASER

UNIVERSITY

STATEMENT OF OPERATIONS and

?

CHANGES IN OPERATING NET ASSETS

.

?

FOR

THE YEAR ENDED MARCH 31, 2004

(thousands of dollars)

REVENUE

Government grants and contracts

Province of British Columbia

Government of Canada

Other governments

Student fees - credit courses

- non-credit courses

-

other

Gifts, grants and contracts

Sale of goods and services

Investment income

Miscellaneous income

Amortization of deferred capital

contributions

EXPENSE

Salaries - academic

-

other instruction and research

- support

staff

Back to top

Total salaries

S

Employee benefits (Note 7)

Travel

and

personnel

costs

Materials and

supplies

Communications

Other operational expenses

Depreciation

Grants to other agencies

Utilities

Renovations and alterations

Scholarships, bursaries and prizes

Contract services

Professional fees

Cost of goods sold

Interest on long-term debt

Equipment rental and

maintenance

EXCESS OF REVENUE OVER EXPENSE

CHANGES IN NET ASSETS

Increase

in specific commitments

Increase in investment

in capital assets

NET CHANGE IN OPERATING EQUITY

2003

$ 165,873

33,541

1,572

62,869

7,252

5,320

21,433

27,608

11,652

3,526

8,018

348,664

73,174

30,682

68,304

172,160

32,235

11,005

13,438

1,351

15,280

23,847

4,023

4,272

5,355

11,846

3,910

10,728

9,336

2,262

2,879

323,927

24,737

(4,232)

(21,055)

(550)?

(16,378)?

$(16,928)

.

?

S

OPERATING NET ASSETS, beginning of year,

OPERATING NET ASSETS, end of year

Page 15

Page 8

Statement 3

S

S

SIMON FRASER UNIVERSITY

STATEMENT OF CHANGES IN NET ASSETS

FOR THE YEAR ENDED MARCH 31, 2004

(thousands of dollars)

Internally

General ?

Restricted for

?

Invested in ?

Restricted for

Operating ?

Specific ?

Capital Assets

?

Endowment

Commitments

?

Principal

2004!,

2003

NET ASSETS, beginning of year

$ ?

(16,928) $

?

74,546 ?

$ ?

127,241 ?

$ ?

97,102

$

?

281,961

$ 253,995

Net change in operating equity

(300)

?

- ?

-

(3

(600)

Endowment contributions

- ?

- ?

- ?

2,665

2,665

2,524

Capital preservation of endowment

?

- ?

-

2,434

2,434

705

5.

?

Capital Assets

tst

Accumulated ?

'. ?

2004

2003

Depreciation

Net

Net

(000)

(000)

(000)

(000)

74,814

$107140

$267,674

$201,977

21,316

9,247

12,069

12,788

23,754

8,337

15,417

15,440

11,666

' ?

4,964

6,702

7,193

24

1

527

•6;979

17,548

14,212

58,508

20,090

38,418

36,049

60,242

23,632

36, 19&

34,437

6.275

4,836

13,836

-

13.836

13.836

94.938

IL

$180.389

5414.549

$340.768

Space in the Central City complex for the Surrey campus, purchased in March 2004, is. included in

buildings. The 429 acres of land in Burnaby is recorded in the financial statements at its 1965

assessed value of $572,000. 78 acres of this land is set aside for development by the SFU

Community Trust. The Centre for Dialogue land is recorded at its 1998 asessed value of

$1,148,000 and the Segal Graduate School of Business land is recorded at its 2002 assessed

value of $3,669,000. Beneficial interest in land held under an educational joint venture agreement

is held by the Great Northern Way Campus Trust.

Buildings - concrete

- wood

Site services

Leasehold improvements

Computing equipment

Equipment & furnishings

Library books

Special collections

Land

Total Capital Assets

Change in investment in capital assets

Amortization of deferred capital

contribution ?

-

-

?

8,453 ?

-

8,453

801

Capital asset acquisitions

? -

-

?

100,219 ?

-

100,219

44

5

Debt ?

-

- ?

(16,844) ?

-

(1 6,8f4)

'

4,03

Deferred contributions

?

-

(41,966)

-

(41 966)

(11,651)

Depreciation ?

-

- ?

(26,438)

-

?

(26,438) (23,847)

Internally imposed restrictions

?

108

IN

NET ASSETS ?

(192)

1,100 ?

-

1,100 ?

23,424

- ?

1,208

5,099

?

29,431

4,282

27,966

CHANGENET

ASSETS, end of year

?

$

?

(17,120) $

75,646 $

?

150,665 $

102,201 ?

P

311,392$

281,961

6. ?

Long Term Debt

S ?

r

2004 ?

2003

I

i1 ?

(000)

Demand Loans

?

$ ?

$ 3,500

Term Loans

?

.

?

.

?

5,2761

?

5,591

Mortgages ?

4,9al ?

2,440

Debentures - Senior unsecured

?

150 0001

?

-

Debentures - Province of BC unsecured

?

16,828,

L

?

21,348

?

(less Sinking Funds) ?

(8_292) ?

(7_799)

?

168,7431

? 25,080

Current Portion ?

(6,176)

? (12,882)

Total Long Term Debt

$162.561 ?

$12.198

Term loans, secured by promissory notes, bear interest rates between 2.43% and 6.54%, and are

due for renewal in December 2004 and January 2005.

Mortgages include CMHC Mortgages and a mortgage on property held in the Great Northern Way

Campus Trust. CMHC Mortgages issued by the Canadian Mortgage and Housing Corporation are

secured by student residence buildings. They bear interest rates between 5.375% to 6.875% and

mature between January 1, 2017 and July 1, 2019 with annual payments including principal and

interest until maturity amount to $248,000. The GNWCT mortgage bears interest at 5.1% per

annum with interest only payments of $131,000 annually until maturity on October 1, 2007.

The University issued $150,000,000 of 5.613% Senior Unsecured Debentures in June 2004. The

S

debentures have semi-annual interest payments and mature June 10, 2043. Net

proceeds of the

issue will be used primarily to finance capital projects. The debentures are neither obligations of,

nor guaranteed by, the Province of British Columbia.

.

Page 14

Page 9

Cost

(000)

$ (324)

18,335

584

$1 8.595

2003

Market

(000)

$ (324)

18,335

584

$1 8.595

Page 13

21,571

19.274

40,845

11.708

52,553

50,633

?

12,029

?

115,215

?

5.057 ?

$1 20.272

4.8

5.4

5.1

5.8

5.2

0

2003

$ ?

24,737

23,847

4,978

(3,328)

(8,018)

17,311

3,229

1,205

63,961

(13,901)

(44,501)

(58,402)

(2,688)

(2,688)

2,871

15,724

$ ?

18,595

OPERATING ACTIVITIES

Excess of revenue over expense

Add (deduct)

Depreciation

Net (increase) decrease in non-cash current assets

Net increase (decrease) in accounts payable and accrued liab

Amortization of deferred capital contributions

Increase in deferred contributions

Endowment contributions

Increase in employees future benefits

CASH PROVIDED BY OPERATING ACTIVITIES

INVESTING ACTIVITIES

Net increase in long term investments

5 ?

Capital asset acquisitions

CASH USED IN INVESTING ACTIVITIES

FINANCING ACTIVITIES

Net proceeds from bond issue

Net debt principal repaid

CASH PROVIDED USED IN FINANCING ACTIVITIES

NET INCREASE IN CASH AND

SHORT TERM INVESTMENTS

CASH AND SHORT TERM INVESTMENTS, beginning of year

CASH AND SHORT TERM INVESTMENTS, end of year

Statement 4

3.

4.

Cash and Short Term Investments

Cash

Short term notes

Bonds maturing under one year

Total Cash and Short Term

Long Term Investments

Long term investments at fiscal year end are comprised of the following:

2003

Cost

Market

Cost

Market

(000)

:000

(000)

(000)

111,286

$115886

$120,272

$120,815

42,072

56-268

34,246

37,476

31,931

25,503

18,621

9,381

11,730

t1,730

11,656

11,656

3,631

3,934

3,752

3,410

2,555-

: '

2,095

2,555

2,065

203,205

215,419

191,102

184,803

5,305

6,871

5,305

6,073

3,765

3,765

3,259

3,259

2i22Th

$226.055J

$199.666

$194.135

The Vancouver Foundation holds a number of endowment funds for the benefit of the University.

These funds totalled $7,338,000 at March 31, 2004 and the portion of $5,305,000 belonging to the

University is included in the University's financial statements. In the fiscal year 2003/04 these

funds generated $422,418 of income (2003 - $612,135) for the University to be used for specific

purposes.

Bonds and Debentures

2003

Cost Effective

Yield

(000) ?

(%)

Segregated Assets

Government bonds

Federal

Provincial

Corporate debentures

Sub-total segregated

Pooled Bond Funds

Indexed - TDQC

Active - CIFD

Sub-total externally held

Internally managed

Total Bonds and Debenti

Bonds and debentures

Canadian equities

Foreign equities

Long term annuity

Pooled balanced fund

Donated hedge fund

Sub Total

Vancouver Foundation

Loans to SFU related entities

Total Long Term

S

SIMON FRASER UNIVERSITY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED MARCH 31, 2004

?

(thousands of dollars)

.

Page 10

1.

b.

C.

SIMON FRASER UNIVERSITY

..

.Capital

Assets

NOTES TO THE FINANCIAL STATEMENTS

Library books

?

10 years

Equipment and furnishings

?

8 years

FOR THE YEAR ENDED MARCH 31, 2004

Computing equipment

?

3 years

Leasehold improvements ?

Term of Lease

Authority and

Purpose

No depreciation is taken on works of art and collections, which include that portion of library assets

considered to have permanent value.

Simon Fraser University is an agent of the Crown and operates under the authority of the University

Act, R.S. Chapter

468. ?

The purpose of the University is to conduct research and deliver a full

d.

Debt Discount and Issue Costs

range of undergraduate, graduate and continuing studies programs.

?

Simon Fraser University is a

not-for-profit entity governed by a Board of Governors, the majority of which are appointed by the

Debt discount and costs related to debt issues are capitalized and amortized over the life of the

provincial government of British Columbia. The academic governance of the University is vested in

debt.

the Senate. The University is a registered charity and is therefore exempt from income taxes under

section

149

of the Income Tax Act.

?

The University receives a significant portion of its revenues

e.

Investments

from the Province of British Columbia.

Short term investments are recorded at the lower of cost or market value.

Summary of Significant Accounting Policies and Reporting Practices

Long term investments, which consist of marketable securities and real estate, are carried at cost

Accounting Method

or, when donated, at their fair market value at the date of the ownership transfer of these assets to

the University. When there has been a decline in the value of an investment that is not considered

The financial statements are prepared following Canadian generally accepted accounting principles

temporary, the investment is written down to net realizable value.

on a non-fund basis as the operations for the entire University have been combined for reporting

purposes.

?

The University follows the accrual basis of accounting.

?

Unrestricted revenue is

Gains and losses on sales of these investments are recognized in the year of disposal and are

Revenue

recorded when

Recognition

receivable and expenditures are recorded when goods or services are received.

0

f.

included

Inventories

in investment income.

Externally restricted contributions for purposes other than endowment or the acquisition of capital

Inventories of supplies kept at Central Stores are recorded at cost.

?

Inventories of merchandise

held for resale in the Bookstore and the Microcomputer Store are recorded at the lower of cost and

assets are deferred and recognized as revenue in the year in which the related expenses are

net realizable value.

incurred. ?

Externally restricted amounts can only be used for purposes designated by the

contributors.

g.

Use of Estimates

Externally restricted capital contributions are recorded as deferred contributions until the amount is

?

The preparation of financial statements in accordance with Canadian generally accepted

invested to acquire capital assets. Amounts invested representing externally funded capital assets

?

accounting principles requires management to make estimates and assumptions that affect the

are then transferred to unamortized deferred capital contributions. Capital contributions are

?

reported amounts of assets and liabilities at the date of the financial statements, and the reported

deferred and amortized to revenue over the life of the related asset. ?

amounts of revenue and expenses during the reporting period. Actual results could differ from

management's best estimates as additional information becomes available in the future. Areas that

Gifts-in-kind are recorded at fair market value on the date of their donation or at nominal value

?

require the greatest degree of estimation include provision for doubtful accounts, depreciation

when the fair market value cannot be reasonably determined, ?

period for capital assets, and actuarial assumptions for employee future benefits.

Capital Assets

?

- ?

h. ?

Related Entities

Capital asset acquisitions are recorded on the statement of financial position at cost, except

?

The University's 25% interest in the Great Northern Way Joint Venture is recorded on a

donated assets which are recorded at fair market value at the date of acquisition. Depreciation is ?

proportionate consolidation basis. Details of other corporations and consortiums, in which Simon

recorded on a straight line basis over the estimated life of the asset as per the schedule below.

?

Fraser University may have a significant interest, are contained in Note 16. These entities are not

consolidated in these financial statements.

Site services ?

50 years

Buildings ?

- concrete ?

50 years

- wood frame

?

30 years

3.

a.

Page 11

?

Page 12