S

S.06-11O

FOR INFORMATION

SIMON FRASER UNIVERSITY

?

MEMORANDUM

TO:

?

Senate

FROM: ?

Alison Watt

Director, University Secretariat

DATE: ?

September 28, 2006 ?

•

SUBJECT:

Annual Financial Statements

Section 32 of the University Act states: "The board must make an annual report of its

transactions to the minister, in which it must set out a balance sheet and a statement of

revenue and expenditure for the year ending on the preceding March 31, and other

particulars the minister may require. A copy of the annual report shall be transmitted

promptly to the senate."

This document is forwarded to Senate for information.

NOTE:

IF YOU DO NOT WISH TO KEEP A COPY OF THE ANNUAL FINANCIAL

?

STATEMENTS, PLEASE RETURN IT TO

?

BOBBIE GRANT, REGISTRAR'S OFFICE, STUDENT SERVICES

0

'-4

z

z

04

:

ii

IL

Ti ?

^3

/

U

CELL

©:g

Mo

ON

Col

All

- ?

--

?

-----:=-

?

____

- ?

3 ?

THE DESIGN GROUP UNIVERSITY RELATIONS PRINTED BY DOCUMENT

4ONS

?

-

?

- ?

-

?

- ? -

a

in

WCUM BS

The University is one of five University members of the Western Canadian

Universities Marine Biological Society (WCUMBS), which operates a

research station at Bamfield, British Columbia. The Society is a not-for-profit

organization incorporated under the Society Act of British Columbia. The

University's operating grant to the Society was $359,000 (2005: $252,000)

and is recorded as an expenditure by the University. There is no

expectation of monetary gain to the University from this venture.

SFU COMMUNITY CORPORATION

The University owns all of the outstanding shares of SFU Community

Corporation. SFU Community Corporation has no business operations

and its sole purpose is to act as the trustee of SFU Community Trust as

described in Notes 2c. and 9.

SF UNIVENTURES CORPORATION

The University owns 100% of the shares of SF Univentures Corporation

(SFUV), which was established to promote technology transfer to the

private sector. The consolidated assets of SFUV are not considered to be

material and are not included in these financial statements.

201S ?

.

FINANCIAL STATEMENTS

Sfrnon ',,or Unreri,y I Fiscal yo,rnndod March 31, 2006

NOTES TO THE FINANCIAL STATEMENTS

1

Authority and Purpose ....... ?

.... ............... ?

.....................

13

2

Summary of Significant Accounting Policies and Reporting Practices

a

?

Accounting ? Method

..................................................... 13

b ?

Related Entities ? ........................................................

13

C

?

Revenue Recognition ?

----------------------------------------------------13

d ?

Capital Assets

?

---------------------------------------------------------13

a

?

Debt Discount and Issue Costs.

?

............................... ...........

?

.

.

14

Investments

?

-----------------------------------------------------------

14

g ?

Inventories ?

------------------------------------------------------------

14

Use of Estimates--------------------------------------------------------

14

3

Cash and Short Term Investments-------------------------------------

14

4

Investments---------------------------------------------------------

14

5

Capital Assets

a ?

Capital Asset Balances----------------------------------------------------15

b ?

Capital Expenditure Commitments

?

------------------------------------------15

6

Long Term

?

Debt ?

----------------------------------------------------15

7

Employee Future Benefits -------------------------------------------

8

Deferred Contributions

9

Deferred Lease Proceeds

I

Entities accounted for by the equity method

a

?

Equity in SFU Community Trust ?

--------------------------------------------16

b ?

SFU Community Trust—Financial Summary-----------------------------------17

10

Internally Restricted for Specific Commitments-------------------------

17

ii

Endowment

--------------------------------------------------------

12

Pension ?

Plans ?

-------------------------------------------------------18

13

Financial Instruments-----------------------------------------------

19

14

Pledges------------------------------------------------------------

19

15

Contingencies------------------------------------------------------

19

16

Canadian University Reciprocal Insurance Exchange-------------------

19

17

Related Entities that are not consolidated

a

TRIOME ?

----------------------------------------------------------------

19

b wcOMBS ? ---------------------------------------------------------------20

C ?

SF0 COMMUNITY CORPORATION -------------------------------------------------20

d

?

SF 0NIVENT000S CORPORATION ?

-------------------------------------------------20

STATEMENT OF MANAGEMENT RESPONSIBILITY

...........................

02

REPORT OF THE VICE-PRESIDENT FINANCE & ADMINISTRATION ............

03

REPORT OF THE AUDITOR

...............................................

..o8

AUDITED STATEMENTS

Statement of Financial Position.... .....................................

.

.

09

Statement of Operations and Changes in Operating Net Assets ..............

10

Statement of Changes in Net Assets........................................

11

Statement of Cash Flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

0

?

S

?

0

01

The University is responsible for the preparation of the

financial statements and has prepared them in accordance

with Canadian generally accepted accounting principles.

The financial statements present fairly the financial position

of the University as at March 31, 2006 and the results of its

operations and its cash flows for the year then ended.

In fulfilling its responsibilities and recognizing the limits

inherent in all systems, the University has developed and

maintains a system of internal control designed to

provide reasonable assurance that University assets are

safeguarded from loss and that the accounting records are

a reliable basis for the preparation of financial statements.

The Board of Governors carries out its responsibility

for review of the financial statements and oversight of

management's performance of its financial reporting

responsibilities principally through its Audit Committee.

The majority of the members of the Audit Committee

are not officers or employees of the University. The Audit

Committee meets with Management, the internal auditor

and the external auditors to discuss the results of audit

examinations and financial reporting matters. The external

auditors have full access to the Audit Committee, with and

without the presence of Management.

The financial statements for the year ended March 31, 2006

have been reported on by BDO Dunwoody LLP, Chartered

Accountants. The Auditors' Report outlines the scope of

their examination and provides their opinion on the fairness

of presentation of the information in the statements.

ik

Dr. Michael Stevenson

PRESIDENT

Pat Hibbitts

VICE-PRESIDENT, FINANCE & ADMINISTRATION

MAY 12, 2006

02

0

I

STATEMENT OF MANAGEMENT RESPONSIBILITY

Simon Fraser University I Fiscal year ended March 31, 2006

The latest actuarial valuation as at December 31, 2004 showed an

actuarial liability of $146,772,000 against market value assets of

$148,825,000, resulting in a surplus of $2,048,000. This surplus is not

available to the University as the University shall not suspend or reduce

its contribution to the pension fund without the prior approval of the

employee organizations. Pursuant to an agreement between the

University and the employee organizations, the portion of the surplus in

excess of 15% of the defined-benefit portion of the above liabilities with

assets taken at market values would be distributed to members. The next

valuation will be at December 31, 2007.

The rate of employer contribution was also increased from 11.44%

to 12.34%, effective January 1, 2005, as indicated by the 2004 actuarial

valuation. Contributions by the employer for the calendar year 2005 were

$8,467,000 (2004: $7,372,000).

The valuation is based on the 1994 Uninsured Pensioner Mortality Table

projected to 2015 using mortality projection scale AA; an investment rate

of return of 6.25%; and an inflation rate of 2.25%.

PENSION PLAN FOR CERTAIN MEMBERS

This plan covers four members of the faculty and staff for whom

contributions were paid to the Teachers Insurance and Annuity Association

and College Retirement Equities fund in 1971, and that have chosen to

remain in the defined contribution plan. University contributions were

$37,400 in calendar year 2005 ($61,500 in 2004).

13.

Financial Instruments

The University's financial instruments consist of cash and short term

investments, accounts receivable, investments, accounts payable and

accrued liabilities and long term debt. It is management's opinion that

the University is not exposed to significant interest, currency or credit risk

arising from these financial instruments. The carrying values of accounts

receivable, accounts payable and accrued liabilities approximate their fair

value due to the relatively short periods to maturity of the instruments. The

fair value of long-term debt approximates the carrying value due to the

nature of the existing terms.

14. Pledges

Pledges made by donors to the University for donations to be received in

future years are estimated at $26,419,000 (2005: $12,794,000). Pledges are

not recorded in the financial statements until the related donations are

received by the University.

15.

Contingencies

Simon Fraser University is the defendant to several unresolved statements of

claims. It is expected that the ultimate outcome of these claims will not have

a material effect on the financial position of the University. Any payouts that

may result from these claims will be recorded in the period when it becomes

likely and determinable.

16. Canadian University Reciprocal Insurance Exchange

The University is a member in a self-insurance co-operative in association

with other Canadian universities to provide property and general liability

insurance coverage. Under this arrangement referred to as the Canadian

University Reciprocal Insurance Exchange (CURIE), the University is

required to share in any net losses experienced by CURIE. The University is

committed to this arrangement until December 31, 2007.

17.

Related Entities that are not consolidated

TRIUMF

Simon Fraser University is a member along with five other universities

in a joint venture called the Tr-Universities Meson Facility (TRIUMF)

located on the University of British Columbia (UBC) campus. TRIUMF is

Canada's National Laboratory for research in Particle Physics. TRIUMF is

not incorporated and each University has an undivided 1/6 interest in all

the assets, liabilities and obligations of TRIUMF, except for the land and

buildings occupied byTRIUMF, which are owned by UBC. The facility and

its operations are funded by federal government grants and the University

makes no direct financial contribution.

Financial Position

(Dollars in thoosan4s)

2006

2005

Total assets

6,059

7,071

Total Liabilities

3,766

4,619

Fund Balances, restricted

2,169

3,047

other

124

(595)

6,059 ? 7,071

19

Results of Operation

Revenue

?

58,197

?

53,628

Expenses

?

58,356

?

54,846

Excess (deficiency) of Revenue over Expenses

?

(159)

?

(1,218)

. ?

.

fl!

VI

Celebrating its 40th anniversary, SFU has earned an international reputation

for innovative teaching, research, athletics, and community outreach. With

three distinctive campuses, more than 700 accomplished tenure-track faculty,

2,500

staff members and nearly 22,000 talented students, SFU consistently

ranks as one of Canada's leading comprehensive universities.

In order to maintain and enhance our reputation and grow

our enrollment we have invested heavily in new buildings,

new faculty and staff for academic programs and we

continue to be very successful at applying and receiving

funds for research.

Revenue for the year was $479 million and expenses

were $455 million leaving a net revenue of which $18 million

represents the increase in investment capital assets. The

remaining $6 million has been allocated to fund activities

for the coming year; details are outlined in this document.

Of particular interest is the use of our Bond issue and

our successful Reaching New Heights campaign which has

allowed us to increase our capital assets by $105 million.

The completion of the Segal Graduate School of Business

at our Vancouver downtown campus and phase one of the

Technology and Applied Sciences Complex are examples.

SFU has hired new faculty and staff to deliver and

support academic programs. We are pleased that the

Provincial Government provided financial resources that

allowed us to secure four year collective agreements with

all our employee groups and associations. The lump sum

components of these agreements are largely responsible

for higher Government funding and higher salary expenses

for the year ending 2006.

Our research activities continue to outpace all areas

of growth with an increase of $7 million this year and an

increase of 66% over the last five years. This allows SFU to

attract the best professors and graduate students which

contribute to the continuing success of this institution.

Pat Hibbitts

VICE-PRESIDENT. FINANCE & ADMINISTRATION

03

0

General Operating is composed of carryover funds for faculties and

departments under a policy that enables them to carry over unspent

budget. It includes unspent balances on specific projects, internally funded

research already in progress, funds set aside for specific provisions and

one-time non-recurring expenditures approved by the Board of Governors.

The Ancillary Enterprises represents accumulated funds held for the

ongoing operations of ancillaries such as the Bookstore, Food Services,

Microcomputer Store, Residences, Parking and Document Solutions.

Capital represents funds that are restricted to capital projects.

Specific purpose represents funds from various sources that are allocated

internally to specific activities.

Funds restricted for long term commitments set aside for future

obligations:

Lease commitment funds provide for obligations entered into for the

occupancy of the University's Harbour Centre facility, which include lease

payments, tenant loan payments and a contribution towards operating

expenses. Lease and tenant loan obligations include annual payments of

$1,140,000, which started in September 1988 increasing to $1,648,000

over the term of the lease, and a termination payment of $8M upon the

expiry of the lease in December 2017 or a discounted equivalent of that

amount at an earlier date.

Self-insurance funds are held to pay self-insured property and liability

losses.

11. Endowment

Endowment consists of restricted donations to the University. Investment

income generated from endowments must be used in accordance with the

various purposes established by the donors or the Board of Governors.

Donors as well as University policy stipulate that the economic value of the

(Do11a" in thosanLr)

2006

2005

Balance, beginning of year

116,050

102,201

Donations

7,767

1,383

Capitalized income and other transfers

Capitalized investment income

3,747

2,977

Equity income for the year, SFU Community Trust

189

175

Other transfers

5,226

5,625

Equity recognized when SFU Community Trust

was deemed to be a controlled entity in 2005

-

3,689

Balance, end of year ?

132,979

?

116,050

S

endowments must be protected by limiting the amount of income that may

be expended, and reinvesting unexpended income.

Income from the University's beneficial interest in SFU Community Trust

was recognized as a direct increase in net assets held as endowment

principal. Described in Note 9, the Trust's sale of 99 year leases results in the

recognition of "deferred lease proceeds" which will be amortized to income

over the remaining terms of the respective leases. Funds realized from the

Trust are invested to generate income for the benefit of the endowment.

12. Pension Plans

The assets and liabilities of pension plans are not reflected in the University's

financial statements.

ACADEMIC PENSION PLAN

The University Pension Plan for Academic Staff generally provides benefits

on a money purchase basis, but includes an option to members who were

in the plan on March 20, 1973 to choose benefits based on years of service,

and the average of the highest sixty (60) consecutive months' salary.

All contributions to the plan are by the employer. Contributions by the

University for the calendar year 2005 were $8,148,000 (2004: $7,478,000).

An amendment to the plan in 1981 and a letter of agreement between

the University and the Faculty Association in 1990 addressed the funding

and the distribution of the formula retirement benefit account. The latest

actuarial valuation for this group as at December 31, 2003 shows an

actuarial liability of $17,380,000 against the actuarial value of assets of

$16,979,000 resulting in an unfunded liability of $401,000. The University

started contributions of $56,400 per year in 2005/2006 towards the

unfunded liability. The valuation is based on the 1994 Uninsured Pensioners

Mortality Table, using an investment rate of return of 6.5% and price

inflation of 3%. The next valuation will be at December 31, 2006.

ADMINISTRATIVE/UNION PENSION PLAN

The University Pension Plan for the Administrative/Union Staff provides

benefits based on years of service and the average of the highest sixty (60)

consecutive months' salary. Pensions are indexed to CPI up to a maximum

of 3% per annum. Under the Pension Plan:

The University's contribution is based on the amounts estimated by

the Actuary and recommended by the Administrative/Union Pension Plan

Trustees to the Board of Governors of the University. The University shall

contribute to the fund such amounts as the Board of Governors

determines are required to fund the retirement benefits. Employees do

not contribute to the Plan.

S

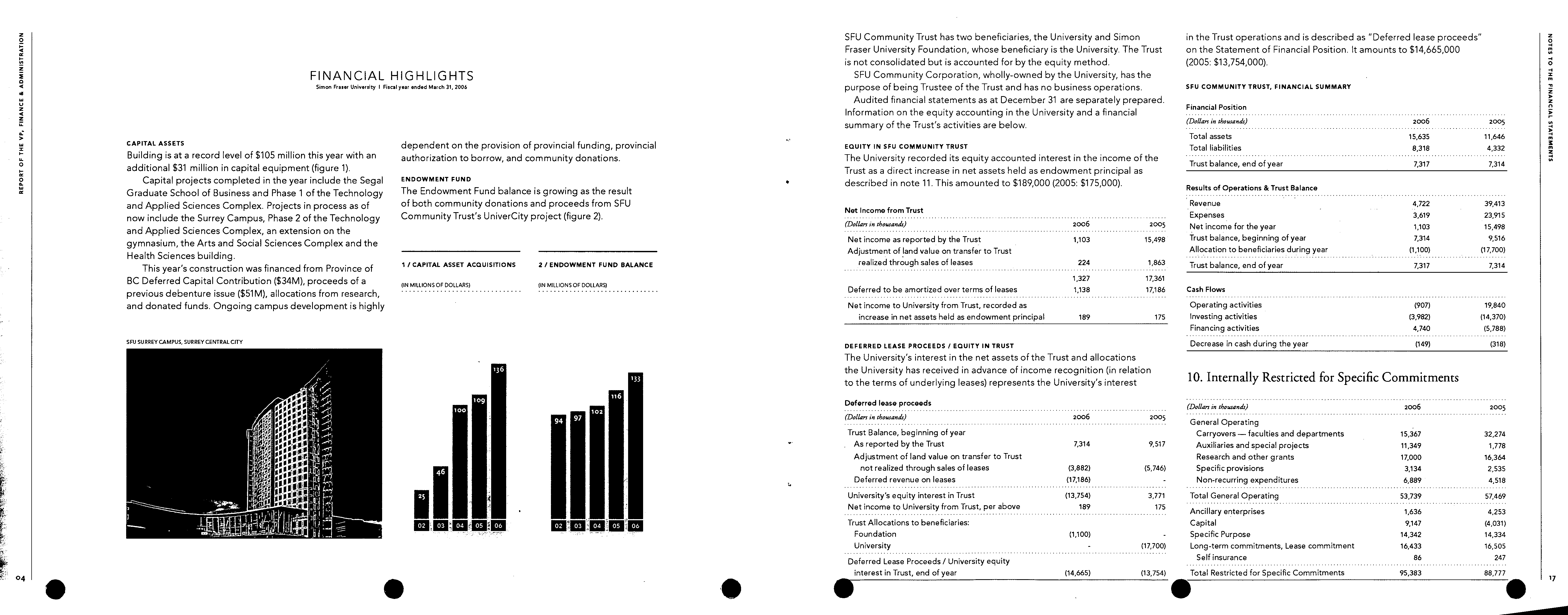

CAPITAL ASSETS

Building is at a record level of $105 million this year with an

additional $31 million in capital equipment (figure 1).

Capital projects completed in the year include the Segal

Graduate School of Business and Phase 1 of the Technology

and Applied Sciences Complex. Projects in process as of

now include the Surrey Campus, Phase 2 of the Technology

and Applied Sciences Complex, an extension on the

gymnasium, the Arts and Social Sciences Complex and the

Health Sciences building.

This year's construction was financed from Province of

BC Deferred Capital Contribution ($34M), proceeds of a

previous debenture issue ($51M), allocations from research,

and donated funds. Ongoing campus development is highly

dependent on the provision of provincial funding, provincial

authorization to borrow, and community donations.

ENDOWMENT FUND

The Endowment Fund balance is growing as the result

of both community donations and proceeds from SFU

Community Trust's UniverCity project (figure 2).

I /CAPITAL ASSET ACQUISITIONS

?

2 / ENDOWMENT FUND BALANCE

(IN MILLIONS OF DOLLARS) ?

(IN MILLIONS OF DOLLARS(

SFU SURREY CAMPUS, SURREY CENTRAL CITY

100

04

FINANCIAL HIGHLIGHTS

Simon Fraser University I Fiscal year ended March 31, 2006

SFU Community Trust has two beneficiaries, the University and Simon

in the Trust operations and is described as "Deferred lease proceeds"

Fraser University Foundation, whose beneficiary is the University. The Trust

on the Statement of Financial Position. It amounts to $14,665,000

is not consolidated but is accounted for by the equity method.

(2005: $13,754,000).

SFU Community Corporation, wholly-owned by the University, has the

purpose of being Trustee of the Trust and has no business operations.

SFU COMMUNITY TRUST, FINANCIAL SUMMARY

Audited financial statements as at December 31 are separately prepared.

Information on the equity accounting in the University and a financial

.

Financial Position

summary of the Trust's activities are below.

l°'

2oo

6

2005

Total assets

15,635

11,646

EQUITY IN SFU COMMUNITY TRUST

Total liabilities

8,318

4,332

The University recorded its equity accounted interest in the income of the

Trust balance, end of year

7,317

7,314

Trust as a direct increase in net assets held as endowment principal as

*

?

described in note 11. This amounted to $189000 (2005: $175,000).

Results of Operations & Trust Balance

Revenue ?

.

4,722

39,413

Net Income from Trust

. ?

Expenses

. ?

.

3,619

23,915

(DolLsrs,n thousands) ?

2006 ? 2005

Net income for the year

1,103

15,498

Net income as reported by the Trust ? 1,103 ?

15,498

Trust balance, beginning of year

7,314

9,516

Adjustment of land value on transfer to Trust

Allocation to beneficiaries during year

(1,100)

(17,700)

realized through sales of leases

?

224 ? 1,863

Trust balance, end of year

7,317

7,314

1,327 ?

17,361

Deferred to be amortized over terms of leases ?

1,138 ?

17,186

Cash

Flows

Net income to University from Trust, recorded as

Operating activities

(907)

19,840

increase in net assets held as endowment principal

?

189 ? 175

Investing activities

(3,982)

(14,370)

Financing activities

4,740

(5,788)

DEFERRED LEASE PROCEEDS / EQUITY IN TRUST

Decrease in cash during the year

(149)

(318)

The University's interest in the net assets of the Trust and allocations

the

to the

University

terms of

has

underlying

received

leases)

in advance

represents

of income

the University's

recognition

interest

(in relation

10. Internally Restricted for Specific Commitments

Deferred

lease

proceeds

(Dollars in thousands)

2006

2005

(Dollars in thousands) ?

2006 ?

2005

General

........,

Operating

?

. .

Trust Balance, beginning of year

Carryovers - faculties and departments

15,367

32,274

As reported by the Trust

?

7,314 ? 9,517

Auxiliaries and special projects

11,349

1,778

Adjustment of land value on transfer to Trust

Research and other grants

17,000

16,364

not realized through sales of leases

? (3,882) ?

(5,746)

Specific provisions

3,134

2,535

Deferred revenue on leases ?

(17,186) ?

-

Non-recurring expenditures

6,889

4,518

University's equity interest in Trust ?

(13,754) ?

3,771

Total General Operating

53,739

57,469

Net income to University from Trust, per above

?

189 ?

175

Ancillary enterprises

1,636

.

.

4,253

Trust Allocations to beneficiaries:

Capital

9,147

(4,031)

Foundation ?

(1,100) ?

-

Specific Purpose

14,342

14,334

University

?

.

?

.

?

.

?

.

- ?

(17,700)

Long-term commitments, Lease commitment

16,433

16,505

Deferred Lease Proceeds / University equity

............

Self insurance

86

interest in Trust, end of year ?

(14,665) ?

(13,754)

Total Restricted for Specific Commitments

95,383

88,777

is

04

C

?

is ?

.

17

SPONSORED RESEARCH

As a comprehensive university, research is a major

component of SFU's mandate. In addition to internally

sponsored research, there is sponsored research funded

by external organizations, including government, Canadian

and international not-for-profit, and industry (figures 3, 4).

ANCILLARY ENTERPRISES

The six ancillary Enterprises provide goods and services

to the University community. Revenues cover operating

expenses, debt service payments and reinvestment for

long term financial viability. Net Assets are designated as

Internally Restricted for Specific Commitments (figures 5, 6).

3 / EXTERNAL RESEARCH REVENUE ?

4/SPONSORED RESEARCH REVENUE

(IN MILLIONS OF DOLLARS)

?

(IN MILLIONS OF DOLLARS)

I!uI

Iii.

9.5

9.8

RESEARCH IN APPLIED SCIENCE

05

.

16

7. Employee Future Benefits

GROUP

EARLY

NON-PENSION

2006

2005

INSURANCE

RETIREMENT

BENEFITS

TOTAL

TOTAL

Opening Balance

5,209

4,862

20,422

30,493

27,481

Current Costs

-

-

993

993

1,212

Interest on benefit obligation

311

291

1,844

2,446

2,177

Adjustment and Amortization

of Net Actuarial Loss

-

-

211

211

567

5,520

5,153

23,470

34,143

31,437

Disbursements

-

406

615

1,021

944

Balance, end of year

?

5,520

?

4,747

?

22,855 ?

33,122 ?

30,493

GROUP INSURANCE

Group insurance is designated for potential requirements related to

self-insured long-term disability plans. Annual premiums are funded from

the general operating funds on a cost of claim plus fee for services basis.

According to Manulife, the insurer, the reserve required at March 31, 2006

to pay disability pension payments is $6,557,000 (2005: $5,492,000). Some

of these employees will be returning to work during the year, so the reserve

of $5,520,000 (2005: $5,209,000) that has been internally designated to fund

this liability is considered adequate.

EARLY RETIREMENT

The early retirement amount represents current and future pension

payments to employees that took early retirement in the mid 1980's and

other employees that receive supplementary pensions. The actuarial

liability at December 31, 2003 was determined by a March 21, 2003 actuarial

valuation based on the 1994 Uninsured Pensioners Mortality table. The

actuarial assumptions used in this valuation are a discount rate of 6.25% and

an inflation rate of 2.5% per annum. The next valuation will be at December

31, 2006. Assets have been internally designated to fund this liability.

NON-PENSION BENEFITS

The non-pension benefits amount represents portions of premiums payable

to current and future retirees for the Medical Services Plan, Extended

Health Benefits and Dental Benefits. The accrued benefit liability for non-

pension benefits is $22,855,000 (2005: $20,422,000) and at March 31, 2006

an amount of $7,524,000 has been internally designated to fund this liability.

An actuarial valuation was done at March 31, 2006 to reflect the changes

in staff and faculty and increase in premiums since the previous valuation

of $23,080,000 at March 31, 2003. The actuarial valuation shows an increase

of $9,166,000, which brings the total obligation to $32,246,000 at March

11

31, 2006. The increase of $9,166,000 will be amortized over the average

remaining service period of active employees. The average remaining

service period of active employees covered by the non-pension benefits as

of March 31, 2006 is 9 years.

The March 31, 2006 valuation is based on the RP-2000 Mortality table.

The actuarial assumptions used in this valuation are a discount rate of 5%,

price inflation at 2.5% per annum, an extended Health benefit trend rate

of inflation plus 6.0% trending down by 0.5% per annum to 3.5%, a Dental

trend rate of inflation plus 2% and an MSP Premium trend rate of 2.5%.

There are no contributions by the employees to fund this benefit. The next

valuation will be March 31, 2009.

8. Deferred Contributions

Deferred contributions represent unspent resources externally restricted for

a particular purpose in a subsequent period.

Changes in deferred contributions

SPONSORED

?

SPECIFIC ?

CAPITAL ?

2006 ?

2005

(Do11a,in rho,sands)

?

RESEARCH- PURPOSE -

? TOTAL ?

TOTAL

Balance, beginning

of the year

27,129

12,319

250.290

289,738

268,130

Add: Contributions

received during the year

59,836

33,581

35,284

128,701

114,570

Less: Transferred to revenue

53,671

32,530

9,208

95,409

92,962

Balance, end of year

33,294

13,370

276,366

323,030

289,738

Under the deferral method of accounting for contributions, restricted

contributions related to expenses of future periods are deferred and

recognized as revenue in the period in which the related expenses are

incurred. The $276,366,000 of deferred capital contribution represents the

unamortized portion of restricted capital advances relating to assets which

were purchased with restricted contributions.

9. Deferred Lease Proceeds / Related Entities accounted for

by the equity method

SFU Community Trust is developing 78 acres of land on Burnaby Mountain

known as "UniverCity." The land was settled on the Trust by the University.

The Trust is a taxable business trust and must pay income taxes on any

taxable income that is not allocated to beneficiaries. The majority of

the development is being accomplished by the sale of 99 year leases to

developers who will develop residential housing.

06

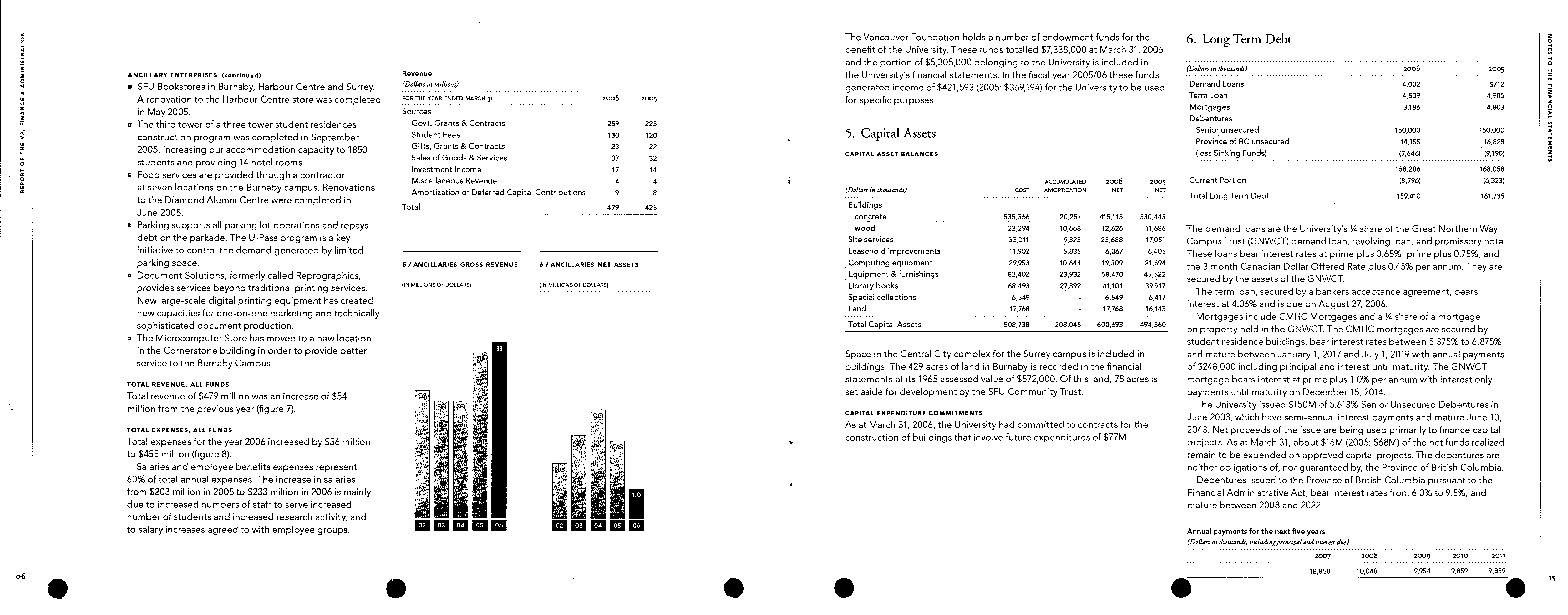

The Vancouver Foundation holds a number of endowment funds for the

6. Long Term Debt

benefit of the University. These funds totalled $7338000 at March 31, 2006

.

and the portion of $5,305,000 belonging to the University is included in

ANCILLARY ENTERPRISES (continued)

Revenue

the University's financial statements. In the fiscal year 2005/06 these funds

(Dollan in thousands) ?

2006 ? 2005

•

SFU Bookstores in Burnaby, Harbour Centre and Surrey.

generated income of $421,593 (2005: $369,194) for the University to be used

Demand Loans

?

.

?

4,002 ? $712

A renovation to the Harbour Centre store was completed

FOR THE YEA R ENDED MARCH 3L

2oo6 ?

2005

for specific purposes.

Term Loan

?

4,509 ? 4,905

in May 2005.

Sources

.

. ?

. ?

. ?

.

Mortgages

?

3,186 ?

4,803

• The third tower of a three tower student residences

Govt. Grants & Contracts

259 ?

225

Debentures

construction program was completed in September

Student Fees

130 ?

120

}.

C ?

?

r' ?

apitai

i

?

Assets

ssets

unsecured ?

150,000 ?

150,000

2005, increasing our accommodation capacity to 1 850

Gifts, Grants & Contracts

23

?

22

,

CAPITAL ASSET BALANCES

Province of BC unsecured ?

14,155 ?

16,828

(less Sinking Funds) ?

(7,646) ?

. (9,190)

.

?

.

students and providing 14 hotel rooms.

Sales of Goods & Services

37 ?

32

• Food services are provided through a contractor

Investment Income

17 ?

14

. ?

. ?

. ?

.

.

168,206

?

168,058

at seven locations on the Burnaby campus Renovations

Miscellaneous Revenue ?

4 ?

4

Amortization of Deferred Capital Contributions ?

9 ?

8

.

ACCUMULATED

?

2006 ?

2005

(DoIIars:nthousands)

?

COST ?

AMORTIZATION ?

NET ?

NET

Current Portion

?

(8,796) ?

(6,323)

to the Diamond Alumni Centre were completed in

..................................

?

.

?

. ?

.

.

Total Long Term Debt ?

159410 ?

161 735

June 2005

Total

479 ?

425

Buildings ?

.

concrete

?

535,366 ?

120,251 ?

415,115 ?

330,445

• Parking supports all parking lot operations and repays

wood

?

. ?

23,294 ?

10,668 ?

12,626 ?

11,686

The demand loans are the University's

14

share ofthe Great Northern Way

debt on the parkade. The U-Pass program is a key

Site services ?

33,011 ?

9,323 ?

23,688 ?

17,051

Campus Trust (GNWCT) demand loan, revolving loan, and promissory note.

initiative to control the demand generated by limited

Leasehold improvements ?

11,992 ?

5,835 ?

6,067 ?

6,405

These loans bear interest rates at prime plus 0.65%, prime plus 0.75%, and

parking space

S /

ANCILLARIES GROSS REVENUE

6 / ANCILLARIES NET ASSETS

Computing equipment ? 29,953 ?

10,644 ?

19,309 ?

21,694

the 3 month Canadian Dollar Offered Rate plus 0.45% per annum. They are

• Document Solutions, formerly called Reprographics,

Equipment & furnishings

?

82,402

?

23,932

?

58,470

?

45,522

secured by the assets of the GNWCT.

provides services beyond traditional printing services

(IN M ILL IONSOF DOLLARS)

Library books ?

68,493

?

27,392 ?

41,101 ?

39,917

The term loan, secured by a bankers acceptance agreement, bears

New large-scale digital printing equipment has created

Special collections ? 6,549 ?

- ?

6,549 ?

6,417

interest at 4.06% and is due on August 27, 2006.

new capacities for one-on-one marketing and technically

Land ?

17,768 ?

- ?

17,768 ?

16,143

Mortgages include CMHC Mortgages and a ¼ share of a mortgage

sophisticated document production.

Total Capital Assets

?

808,738 ?

208,045 ?

600,693 ?

494,560

on property held in the GNWCT. The CM HC mortgages are secured by

The Microcomputer Store has moved to a new location

student residence buildings, bear interest rates between 5.375% to 6.875%

in the Cornerstone building in order to provide better

Space in the Central City complex for the Surrey campus is included in

and mature between January 1, 2017 and July 1, 2019 with annual payments

service to the Burnaby Campus.

I

buildings. The 429 acres of land in Burnaby is recorded in the financial

of $248,000 including principal and interest until maturity. The GNWCT

statements at its 1965 assessed value of $572,000. Of this land, 78 acres is

mortgage bears interest at prime plus 1.0% per annum with interest only

TOTAL REVENUE, ALL FUNDS

Total revenue of $479 million was an increase of $54

r ?

.

set aside for development by the SFU Community Trust.

payments until maturity on December 15, 2014.

million from the previous year (figure

I).

r ?

r

?

. ?

.

CAPITAL EXPENDITURE COMMITMENTS

The University issued $150M of 5.613% Senior Unsecured Debentures in

:.

June 2003, which have semi-annual interest payments and mature June 10,

TOTAL

EXPENSES

ALL FUNDS

As at March 31 2006 the University had committed to contracts for the

2043 Net proceeds of the issue are being used primarily to finance capital

Total expenses for the year 2006 increased by $56 million

1

construction of buildings that involve future expenditures of $77M.

projects As at March 31 about $16M (2005 $68M) of the net funds realized

to $455 million (figure 8)

I

remain to be expended on approved capital projects The debentures are

Salaries and employee benefits expenses represent

neither obligations of nor guaranteed by the Province of British Columbia

60% of total annual expenses The increase in salaries

I

Debentures issued to the Province of British Columbia pursuant to the

from $203 million in 2005 to $233 million in 2006 is mainly

I

.

Financial Administrative Act bear interest rates from 6.0% to 9.5%, and

due to increased numbers of staff to serve increased

' ?

j

mature between 2008 and 2022

number of students and increased research activity, and

Ai

to salary increases agreed to with employee groups.

Annual payments for the next five years

(Del/an in thousands, inch'dingpnndpal

and inte,-at due)

2007 ?

2008 ?

2009 ?

2010 ?

2011

18,858 ?

10,048 ?

9,954 ?

9,859 ?

9,859

.

.

.

?

.

15

Estimated

(Tone In years)

useful life

3. Cash and Short Term Investments

Site services

50

2006

2005

Buildings

(Dollars in thoRsands)

?

COST

MARKET

COST

MARKET

wood

concreteframe

3050

Short

Cash ?

term notes ?

69,809(9,034)

69,809(9,034)

113,7364,475

113,736

4,475

Library

Equipment

booksand

furnishings

10

8

Bonds maturing under one year

?

12,530

12,530

4,888

4,888

Computing equipment

3

Total Cash and Short Term

?

73,305

73,305

123,099

123,099

Leasehold improvements

Term of Lease

14

No amortization is taken on land, works of art and collections, which

include that portion of library assets considered to have permanent value,

as they are considered to have an unlimited useful life.

DEBT DISCOUNT AND ISSUE COSTS

Debt discount and costs related to debt issues are capitalized and

amortized over the life of the debt.

INVESTMENTS

Short term investments are recorded at the lower of cost or market value.

Long term investments, in marketable securities, are carried at cost

or, when donated, at their fair market value at the date of the ownership

transfer to the University. When there has been a decline in the value of

an investment that is not considered temporary, the investment is written

down to net realizable value.

Gains and losses on sales of investments are recognized in the year of

disposal and are included in investment income.

INVENTORIES

Inventories of supplies kept at Central Stores are recorded at cost.

Inventories of merchandise held for resale in the Bookstore and the

Microcomputer Store are recorded at the lower of acquisition cost and net

realizable value.

USE OF ESTIMATES

The preparation of financial statements in accordance with Canadian

generally accepted accounting principles requires management to make

estimates and assumptions that affect the reported amounts of assets

and liabilities at the date of the financial statements, and revenue and

expenses during the reporting period. Significant areas requiring the use

of management estimates include the impairment of assets, provision for

doubtful accounts, amortization period for capital assets, and actuarial

assumptions for employee future benefits and pension plans. Actual results

could differ from management's best estimates as additional information

becomes available in the future.

4. Investments

Long Term Investments

2006

2005

(Dollars in tholssands)

COST

MARKET

COST

MARKET

Bonds and debentures

125,100

126,905

125,963

128,673

Canadian equities

78,562

109,664

58,637

77,105

Foreign equities

42,310

45,569

37,356

37,763

Long term annuity

11,919

11,919

11,827

11,827

Vancouver Foundation

5,305

7,432

5,305

6,892

Donated hedge fund

2,000

2,003

2,000

2,014

Loans to SFU related entities

-

-

2,292

2,292

Total Long Term Investments

265,196

303,492

243,380

266,566

Bonds and Debentures

Analysis

(Dollars in rhoASana5)

Segregated Assets:

Government bonds

• Federal + guaranteed

• Provincial + municipal

Corporate debentures

Sub-total segregated

Indexed Bond Fund

Sub-total externally managed

Internally managed Bonds

Total Bonds and Debentures

.

Expenses

?

ACADEMIC QUADRANGLE, BURNABY CAMPUS

(Dollars in millions)

FOR THE YEAR ENDED MARCH 31:

?

2006 ?

2005

Sources

Salaries

?

233 ?

203

Employee Benefits

?

42

?

37

Supplies & Services

?

100 ?

85

Amortization of Capital Assets

?

32 ?

29

Cost of Goods Sold

?

11 ?

10

Scholarships, Bursaries

?

23 ?

22

Interest on Long Term Debt

?

8 ?

9

Grants to Other Agencies

?

6 ?

5

Total

?

455 ?

400

7/TOTAL REVENUE 2006

?

8/TOTAL

EXPENSES 2006

(IN MILLIONS OF DOLLARS)

?

(IN MILLIONS OF DOLLARS)

SALARIES

SUPPLIES & SERVICES

.M.. OF

-

CAMTAL ASSETS

DI

ll

.......

.

COST

OF GOODS

SOLD

8

.............

-;;-

.

•)O7

2006

2005

COST

MARKET

COST

MARKET

GOVI GRUnTS

&

CONTRACTS

26,833

26,921

25,209

25,722

19,432

20,196

26,639

27,586

1-23

46,265

47,117

51,848

V

53,308

17,913

18,017

15,848

15,838

STUDENT FEES

64,178

65,134

67,696

69,146

57,680

58,161

54,281

55,491

? *

................

SEllS

OF GOODS

121,858

123,295

121,977

124,637

&SERVIcGS

INVESTMENT INCOME

3,242

3,610

3,986

4,036

4

?

............... .... ...........

?

MIEC

9

?

...............

TOTAL

125,100

126,905

125,963

128,673

To the Members of the Board of Governors of Simon

Fraser University, and to the Minister

of Advanced

Education, Province of British Columbia:

We have audited the Statement of Financial Position

of Simon Fraser University as at March 31, 2006 and the

Statements of Operations and Changes in Operating

Net Assets, Changes in Net Assets, and Cash Flows for

the year then ended. These financial statements are

the responsibility of the University's management. Our

responsibility is to express an opinion on these financial

statements based on our audit.

We conducted our audit in accordance with Canadian

generally accepted auditing standards. Those standards

require that we plan and perform an audit to obtain

reasonable assurance whether the financial statements are

free of material misstatement. An audit includes examining,

on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also

includes assessing the accounting principles used and

significant estimates made by management, as well as

evaluating the overall financial statement presentation.

In our opinion, these financial statements present fairly, in

all material aspects, the financial position of the University

as at March 31, 2006 and the results of its operations and

its cash flows for the year then ended in accordance with

Canadian generally accepted accounting principles.

BDO Dunwoody

LLP

CHARTERED ACCOUNTANTS

VANCOUVER, BRITISH COLUMBIA

MAY 12, 2006

NOTES TO THE FINANCIAL STATEMENTS

Simon Fraser University I Fiscal year ended March 31, 2006

AUDITOR'S REPORT

BOO Onwoody LLP, Chartered Accountants, Vancouver, British CoI,,,,,bi,

08

1. Authority and Purpose

Simon Fraser University is an agent of the Crown and operates under

the authority of the University Act, R.S. Chapter 468. The purpose of the

University is to conduct research and deliver a full range of undergraduate,

graduate and continuing studies programs. Simon Fraser University is a

not-for-profit entity governed by a Board of Governors, the majority of

which are appointed by the provincial government of British Columbia.

The academic governance of the University is vested in the Senate. The

University is a registered charity and is therefore exempt from income

taxes under section 149 of the Income Tax Act. The University receives a

significant portion of its revenues from the Province of British Columbia.

2.

Summary of Significant Accounting Policies and

Reporting Practices

ACCOUNTING METHOD

The financial statements are prepared in accordance with Canadian

generally accepted accounting principles for not-for-profit organizations

on a non-fund basis, as the operations for the entire University have been

combined for reporting purposes. These principles are consistent with

those used in prior years.

The deferral method of accounting for contributions is used. Results are

reported in the operating fund, special purpose fund and capital fund.

Revenues and expenses are recorded on a gross and accrual basis.

RELATED ENTITIES

The University's 25% interest in the Great Northern Way Campus Trust is

recorded on a proportionate consolidation basis. Simon Fraser University

Foundation is consolidated in the accounts of the University. The SFU

Community Trust is recorded based on the equity method as described

in Note 9.

Details of other corporations and consortiums, in which the University

may have a significant interest, are contained in Note 17. These entities are

not consolidated in these financial statements as the net assets are not

contemplated to be, and are not, readily realizable by the University.

REVENUE RECOGNITION

Operating government grants not restricted in use are recognized when

received or receivable. Such grants, if contributed for a future period, are

deferred and reported as deferred contributions until that future period.

Other unrestricted revenue, including student fees and sales of goods

and services, are reported as revenue at the time the services or products

are provided. Unrestricted contributions are recognized as revenue when

received.

Externally restricted contributions - grants and donations - are

reported as revenue depending on the nature of restrictions on the use

of the funds by the contributors.

Contributions for specific purposes other than endowment or the

acquisition of capital assets are recorded as deferred contributions

and recognized as revenue in the year related expenses are incurred.

Contributions restricted for capital purposes are recorded as deferred

contributions until the amount is invested in capital assets.

If the capital asset acquired is land or a special collection item, the

amount is recorded as a direct increase to net assets invested in

capital assets.

• If the capital asset has a limited life, the amount invested is

recorded as a deferred capital contribution and amortized over

the useful life of the asset to net assets invested in capital assets.

Amortization of capital contributions is recorded on a straight-line

basis over the estimated life of the related assets and commences

in the year following acquisition or substantial completion of

construction.

Endowment contributions, matching contributions and investment

income allocated for endowment capital preservation are recognized

as direct increases in net assets held for endowments in the period in

which they are received or earned.

Gifts-in-kind are recorded at fair market value on the date of their

donation or at nominal value when the fair market value can not be

reasonably determined.

CAPITAL ASSETS

Capital asset acquisitions are recorded on the statement of financial

position at cost. Donated assets are recorded at fair market value at the

date of acquisition. Amortization of capital assets is recorded on a straight

line basis over the estimated life of the asset and commences in the year

following acquisition or substantial completion of construction.

.

?

9

?

0

?

0

S

4

0

0

0

4

12

0

(Dollar-s in thousands)

YEAR ENDED MARCH

31, 2006:

Operating Activities

Net Revenue for the Year

Items not involving cash:

Amortization of deferred capital contributions

Amortization of capital assets

Amortization of debt discount and issue Costs

Employee future benefits

Changes in non-cash working capital balances

Equity from SFU Community Trust

Accounts receivable

Inventories

Prepaid expenses

Accounts Payable and accrued liabilities

Deferred contributions

Cash Provided by Operating Activities

Investing Activities

Net increase in long term investments

Capital assets purchased

Endowment contributions

Distributions from SFU Community Trust

Cash Used in Investing Activities

Financing Activities

Deferred capital contributions

Long term debt proceeds

Debt principal repaid

Cash Provided Used in Financing Activities

Net Increase (Decrease) in Cash and Short Term Investments

Cash and Short Term Investments, beginning of year

Cash and Short Term Investments, end of year

2006

?

2005

23,522

25,035

(9,208)

(8,312)

31,758

29,122

288

289

2,629

3,012

(189)

(175)

48,800

48,971

(14,124)

(3,529)

(300)

281

(111)

341

15,160

19,232

7,216

(6,561)

56,641

58,735

(21,816)

(31,105)

1137,8911

(109,133)

16,740

9,985

1,100

18,500

(141,867)

(111,753)

35,284

36,481

3,290

712

(3,142)

(1397)

35,432

35,796

149,794 1

(17,222)

123,099

140,321

73,305

123,099

STATEMENT OF CASH FLOWS

Simon Fraser University 2005/06

.

4

1J

STATEMENT OF FINANCIAL POSITION

Simon Fraser University 2005/06

a

(Dollars in thousands)

AS AT MARCH 31, 2006:

Notes

2006

2005

Assets

Current Assets:

Cash and short-term investments

3

73,305

123,099

Accounts receivable

31,050

16,926

Inventories

1,973

1,673

Prepaid expenses

3,540

3,429

109,868

145,127

Investments

4

265,196

243,380

Capital assets

5

600,693

494,560

Unamortized debt discount and issue costs

10,497

10,785

Total assets

986,254

893,852

Liabilities and Net Assets

Current Liabilities:

Accounts payable and accrued liabilities

56,868

41,708

Current portion of long term debt

6

8,796

6,323

65,664

48,031

Employee future benefits

7

33,122

30,493

Long-term debt

6

159,410

161,735

Deferred contributions

8

46,664

39,448

Deferred contributions related to capital assets

8

276,366

250,290

Deferred lease proceeds

9

14,665

13,754

595,891

543,751

Net Assets:

Operating

(20,331)

(18,892)

Internally Restricted for specific commitments

10

95,383

88,777

Invested in capital assets

182,332

164,166

257,384

234,051

Endowment

11

132,979

116,050

390,363

350,101

Total Liabilities and Net Assets

986,254

893,852

The accompanying notes on pages 13-20 are an integral part of those financial statements.

Approved:

?

S

Rasul

CHAIR, BOARD OF GOVERNORS

P Hibbitts

VICE-PRESIDENT, FINANCE & ADMINISTRATION

.

.

•°

Z

4

a

a

4

'I

STATEMENT OF OPERATIONS AND CHANGES IN OPERATING NET ASSETS

SimonFraser Univosty 2005/06

(Dollars

in thousands)

FOR THE YEAR ENDED MARCH

?

2006:

29

2005

Revenue

Government grants and contracts:

Province of British Columbia

209,920

175,354

Government of Canada

46,916

48,208

Other governments

2,209

1,684

Student fees - Credit courses

113,604

103,741

Non-credit courses

7,984

8,312

Other

8,696

.

? 7,330

Gifts, grants and contracts

22,516

22,076

Sales of goods and services

36,949

31,835

Investment income

16,868

13,509

Miscellaneous income

4,138

4,260

Amortization of deferred capital contributions

9,208

8,312

479,008

424,621

Expense

Salaries - Academic

87,978

78,794

Other instruction and research

51,486

42,506

Support staff

93,972

81,921

Total salaries

233,436

203,221

Employee benefits

42,315

36,708

Travel and personnel expenses

15,745

12,855

Materials and supplies

17,030

14,320

Communications

1,468

1,441

Other operational expenses

22,785

19,213

Amortization of capital assets

31,758

29,122

Grants to other agencies

5,978

4,836

Utilities

7,130

5,307

Renovations and alterations

9,751

5,569

Scholarships, bursaries and prizes

22,896

21,672

Contract services

7,276

4,721

Professional fees

14,613

17,938

Cost of goods sold ?

.

11,092

10,177

Interest on long-term debt

7,933

8,749

Amortization of bond discount and issue costs

288

289

Equipment rental and maintenance

3,992

3,448

455,486

399,586

Net Revenue for the Year

23,522

25,035

Changes in Net Assets

Increase in net assets restricted for specific commitments

(6,606)

(13,131)

Increase in investment in capital assets

(18,166)

(13,501)

Equity earnings transferred to endowment

(189)

11751

Net change in operating net assets

(1,439)

11,7721

Operating net assets, beginning of year

(18.892)

(17.1201

STATEMENT OF CHANGES IN NET ASSETS

Simon Freest University 2005/06

(Dollars

in thousands)

Internally Restricted for

Restricted for

FOR THE YEAR ENDED MARCH 31, 2006:

General Operating

Specific Commitments

Invested in Capital Assets

Endowment Principal

Total

Net Assets, beginning of year

(18,892)

88,777

164,166

116,050

350,101

Changes for the Year

Net Revenue for the Year

23,522

-

-

-

23,522

Transfers

Increase in restricted for specific commitments

(6,606)

6,606

Increase in investment in capital assets

(18,166)

-

18,166

-

-

Equity earnings transferred to endowment

(189)

-

-

189

-

(24,961)

6,606

18,166

189

-

Endowment transactions

Contributions

-

-

-

7,767

7,767

Capitalized income and other transfers

-

-

-

8,973

8,973

-

-

-

16,740

16,740

Net Assets, end of year

120,3311

95,303

182,332

132,979

390,363

Represented by:

Employee Future benefits (Note 7)

Funded liability

17,791

Accrued liability

(33,122)

Unfunded portion

(15,331)

Vacation Pay, accrued but not funded

(5,000)

Operating Net Assets (deficit)

(20,331)

S

C

a

a

.4

-4

2

-4

10

0

?

0

?

0

??

..

?

. is

?

LII